Step-by-Step Guide to Applying the Arm's Length Principle for Transfer Pricing, UAE

Transfer Pricing (TP) is a fundamental component of corporate tax compliance in the UAE.

It ensures that transactions between related parties are conducted as if they were between independent entities, reflecting the true market value. This principle helps prevent profit shifting and ensures fair taxation.

What is the Arm’s Length Principle ?

The Arm’s Length Principle

is a cornerstone of transfer pricing under Article 34 of the UAE Corporate Tax Law. It ensures that transactions between Related Parties or Connected Persons are priced as if they were conducted between independent parties under similar circumstances.

Here's a simplified explanation - The Arm’s Length Principle requires that the prices and conditions of transactions between related entities (like members of the same corporate group) reflect what would have been agreed upon if the entities were independent and dealing at arm's length. This means considering what price two unrelated parties would agree upon in similar circumstances.

3 Key Steps in applying the Arm's Length Principle

Three Key Steps to Applying the Arm's Length Principle for Controlled Transactions

Step 1: Identify and Analyze - Identify and analyze related parties, connected persons, relevant transactions, and perform a comparability analysis accordingly.

Step 2: Select Transfer Pricing Method - Choose the most appropriate Transfer Pricing method to apply to the transactions.

Step 3: Determine the Arm’s Length Price - Calculate the Arm’s Length Price based on the chosen method, ensuring it reflects what independent parties would agree upon under similar circumstances.

In this article, we will discuss Step 1: How to Identify Related Parties, Connected Persons, relevant transactions, and arrangements, and perform a comparability analysis accordingly.

This step involves four key aspects:

1. Identify Related Parties.

2. Identify Relevant Transactions and Arrangements.

3. Identify the Commercial and Financial Relations Between Related Parties.

4. Analyze the Economically Relevant Characteristics (Comparability Factors) of the Transaction.

These aspects are essential for choosing and applying the most appropriate Transfer Pricing method.

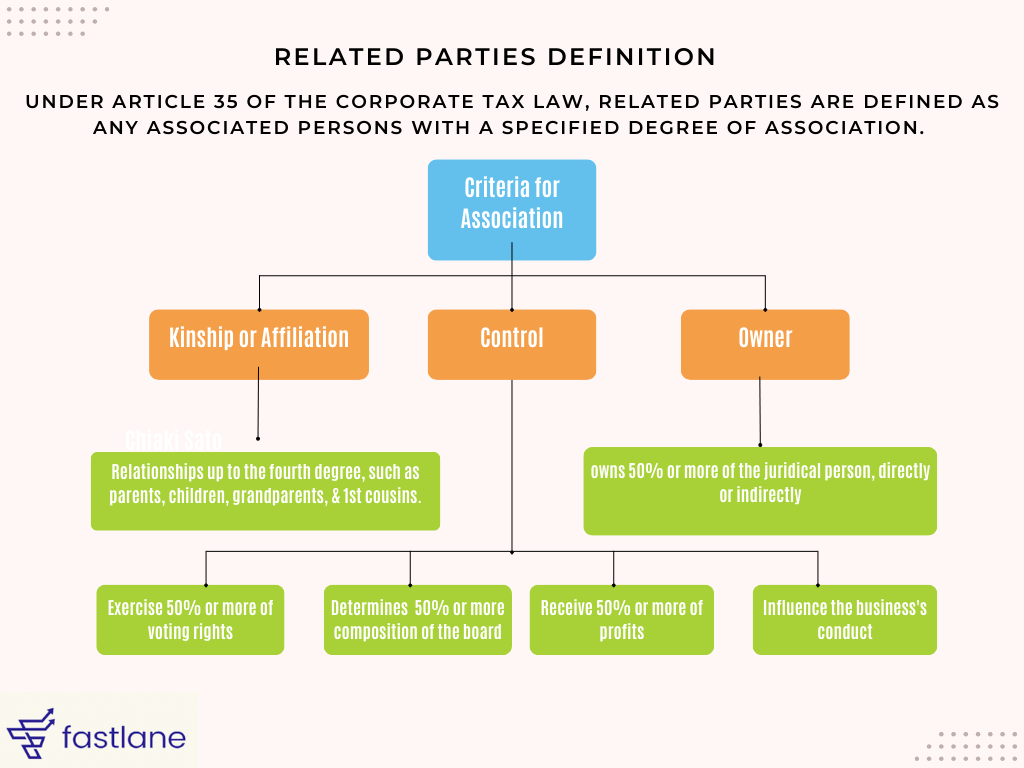

How to Identify Related Parties

Related Parties: Entities that are connected through ownership, control, or family relationships.

- Kinship includes relationships up to the fourth degree, such as parents, children, grandparents, and first cousins. - Ownership involves direct or indirect control of 50% or more in a juridical person. - Control refers to having significant influence over another person’s business and affairs.

Identify Relevant Transactions and Arrangements

Relevant Transactions - Transactions that involve the transfer of goods, services, or financial resources between related parties.

Financial and Commercial Relations: Financial and commercial relations between related parties must be examined to understand the nature of the controlled transactions.

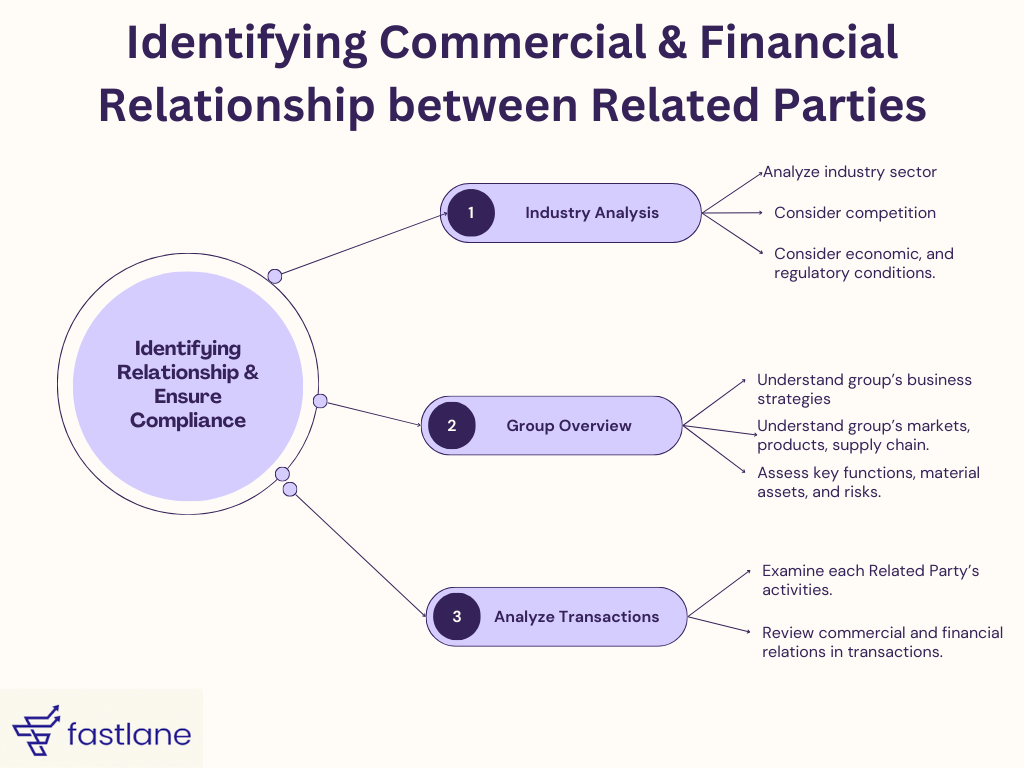

Identifying Commercial & Financial Relationship between Related Parties

When independent parties transact with each other, the conditions of their commercial and financial relations (for example, the price of goods transferred, or services provided and the conditions of the transfer or provision) ordinarily are determined by

market forces and negotiations.

On the other hand, Related Parties or Connected Persons may not be subject to the same external market forces in their dealings and may be influenced by the relationship between the parties involved.

The application of the Arm’s Length Principle hinges on understanding the conditions that independent parties would agree upon in similar circumstances.

Here’s a simplified process to identify these relations and ensure compliance:

Industry Analysis: Start by analyzing the industry sector (e.g., mining, pharmaceuticals, luxury goods) and the factors influencing performance (competition, economic, and regulatory conditions).

Group Overview: Understand the group’s response to industry factors, including business strategies, markets, products, supply chain, key functions, material assets, and risks assumed.

Analyze Transactions: Examine what each Related Party does and their commercial or financial relations as expressed in transactions.

Analysis of Comparability Factors

After identifying the relevant commercial and financial relations, the comparability factors are analysed in detail below.

1. Contractual terms

2. Functional analysis

3. Risk framework

1. Contractual Terms of the Transaction

Overview:

Contracts formalize the commercial and financial relations between parties, outlining responsibilities, obligations, rights, risks, pricing, and terms of the goods or services covered.

Key Points:

- Written Contracts: These are the starting point for understanding transactions. They describe the responsibilities, risks, and anticipated outcomes.

- Supplementary Information:Written contracts alone may not provide all necessary details.

- Additional information can be found in emails, meeting notes, and other correspondences.

Actual Conduct vs. Written Contract:

If actual conduct differs from the written contract, analyze the conduct to determine the true nature of the transaction.

No written contract? Use actual conduct to identify transaction characteristics (functions performed, assets used, and risks assumed).

2. Functional Analysis

Overview:

Involves assessing the economically significant activities, responsibilities, assets, and risks associated with a transaction to ensure comparability between controlled and uncontrolled transactions.

- Assets Used:Type and nature of assets involved in the transaction.

- Risks Assumed: Higher risks should correlate with higher returns. - The allocation of risks affects transaction pricing and comparability with similar uncontrolled transactions.

Case Study - Comparability Factors at Starbucks Corp, UAE

Overview:

Starbucks Corporation, a leading coffeehouse chain, operates globally and ensures its transfer pricing aligns with the Arm’s Length Principle. This case study examines how Starbucks manages its transfer pricing through contractual terms, functional analysis, and risk framework.

Contractual Terms of the Transaction

1. Written Contracts:

- Describe responsibilities, risks, and outcomes between Starbucks' entities.

- Govern the supply of coffee beans from Starbucks Trading Company to global outlets.

2. Supplementary Information:

- Includes emails, meeting notes, and internal reports for comprehensive analysis.

3. Actual Conduct vs. Written Contract:

- Aligns actual conduct with written contracts. Discrepancies are analyzed to determine true transaction nature. - In the absence of written contracts, actual conduct identifies transaction characteristics.

Understanding and analyzing the contractual terms, functional analysis, and risk framework helps Starbucks ensure that its transfer pricing aligns with the Arm's Length Principle.

This process involves identifying commercial and financial relations, accurately delineating transactions, and performing a comparability analysis.

By doing so, Starbucks can select the most appropriate transfer pricing method, ensuring compliance and fair profit allocation across its global operations.

Conclusion

1. Ensures Fair Taxation: The Arm's Length Principle ensures that transactions between related parties reflect true market value, preventing profit shifting and ensuring fair taxation.

2. Structured Approach: The process involves identifying related parties, selecting an appropriate transfer pricing method, and determining the arm's length price based on comparable independent transactions.

3. Regulatory Compliance: By adhering to these steps, businesses can comply with Transfer Pricing requirements, UAE Corporate Tax Law, ensuring their transactions are transparent and accurately reflect economic realities.

How Fastlane Can Help with Transfer Pricing Compliance for UAE:

1. Comprehensive Transfer Pricing Study:

- In-Depth Analysis:Fastlane conducts thorough functional and comparability analyses to ensure compliance with the Arm's Length Principle.

- Documentation Support: We help prepare the necessary documentation, ensuring all transactions meet the stringent requirements of the UAE Corporate Tax Law.

2. Method Selection and Price Determination:

- Expert Methodology: Fastlane assists in selecting the most appropriate Transfer Pricing method tailored to your specific transactions.

- Accurate Pricing: We determine the Arm’s Length Price, ensuring it reflects what independent parties would agree upon under similar circumstances, thus ensuring fair taxation and compliance.

Created with

Login or sign up to start learningLogin to start learning