Calculating Corporate Tax for a Free Zone Business in UAE

Corporate tax is a direct tax levied on the taxable income of corporations and other businesses. In the UAE, corporate tax applies to companies, certain partnerships, unincorporated entities, and even natural persons conducting business activities. In this article, we will go through how to calculate corporate tax for Free Zone Persons (FZPs) in UAE

How do Free Zone Persons benefit from Corporate Tax rules?

Free Zone Persons (FZPs) are entities incorporated, established, or registered in one of the UAE’s Free Zones. These include Free Zone companies and branches that meet specific conditions set by the UAE Corporate Tax rule.

To support the significance of Free Zones, the UAE Corporate Tax rules allow Free Zone companies and branches that meet specific conditions to enjoy a 0% Corporate Tax rate on certain qualifying activities and transactions.

What conditions must Free Zone Persons (FZPs) meet to qualify for the 0% Corporate Tax rate?

A Qualifying Free Zone Person (QFZP) is a Free Zone entity that meets the conditions outlined in Article 18 of the Corporate Tax Law. For detailed information on these conditions, refer to our article on "How to Claim a 0% Corporate Tax Rate in a Free Zone, UAE"

Understanding Corporate Tax Rates for Free Zone Persons

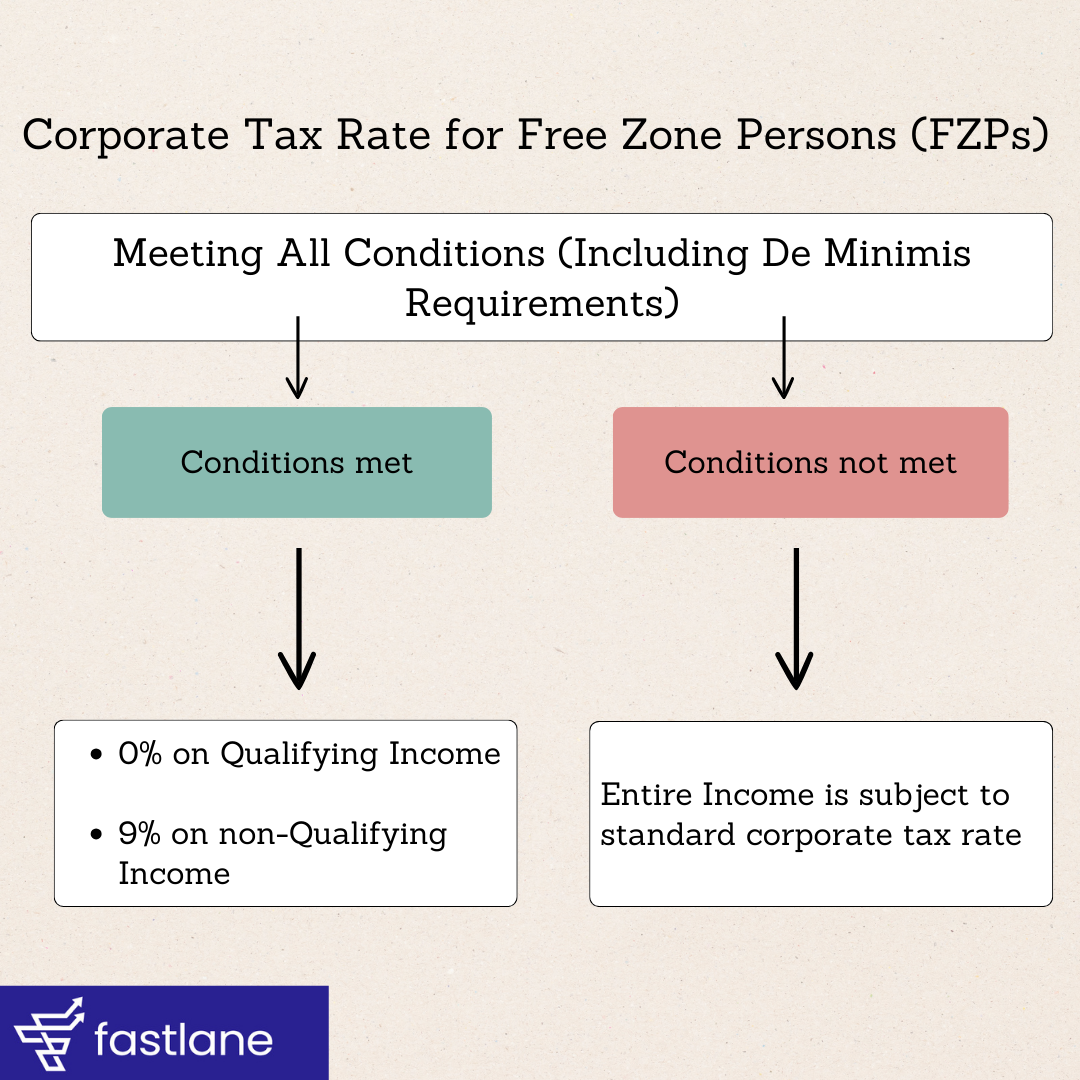

If you're a Free Zone Person meeting all the necessary conditions (including the de minimis requirements), you get to enjoy some significant tax benefits.

Here's how it works:

- 0% Corporate Tax rate on Qualifying Income

- 9% Corporate Tax rate on Taxable Income that is not Qualifying Income.

However, it's important to note that a QFZP is not entitled to the 0% Corporate Tax rate on its first AED 375,000 of Taxable Income.

What is Qualifying Income?

Qualifying Income is income derived from specific categories, including:

- Transactions with other Free Zone Persons who are the Beneficial Recipients (excluding Revenue from Excluded Activities).

- Transactions related to Qualifying Activities (excluding Revenue from Excluded Activities).

- Qualifying Income from Qualifying Intellectual Property.

- Other sources, provided the QFZP satisfies the de minimis requirements.

However, revenue from the following sources doesn't qualify:

- Foreign Permanent Establishments

- Domestic Permanent Establishments

- Immovable Property (unless it's Commercial Property in a Free Zone dealing with another Free Zone Person)

- Intellectual property that isn't classified as Qualifying Intellectual Property

Taxable Income That Is Not Qualifying Income

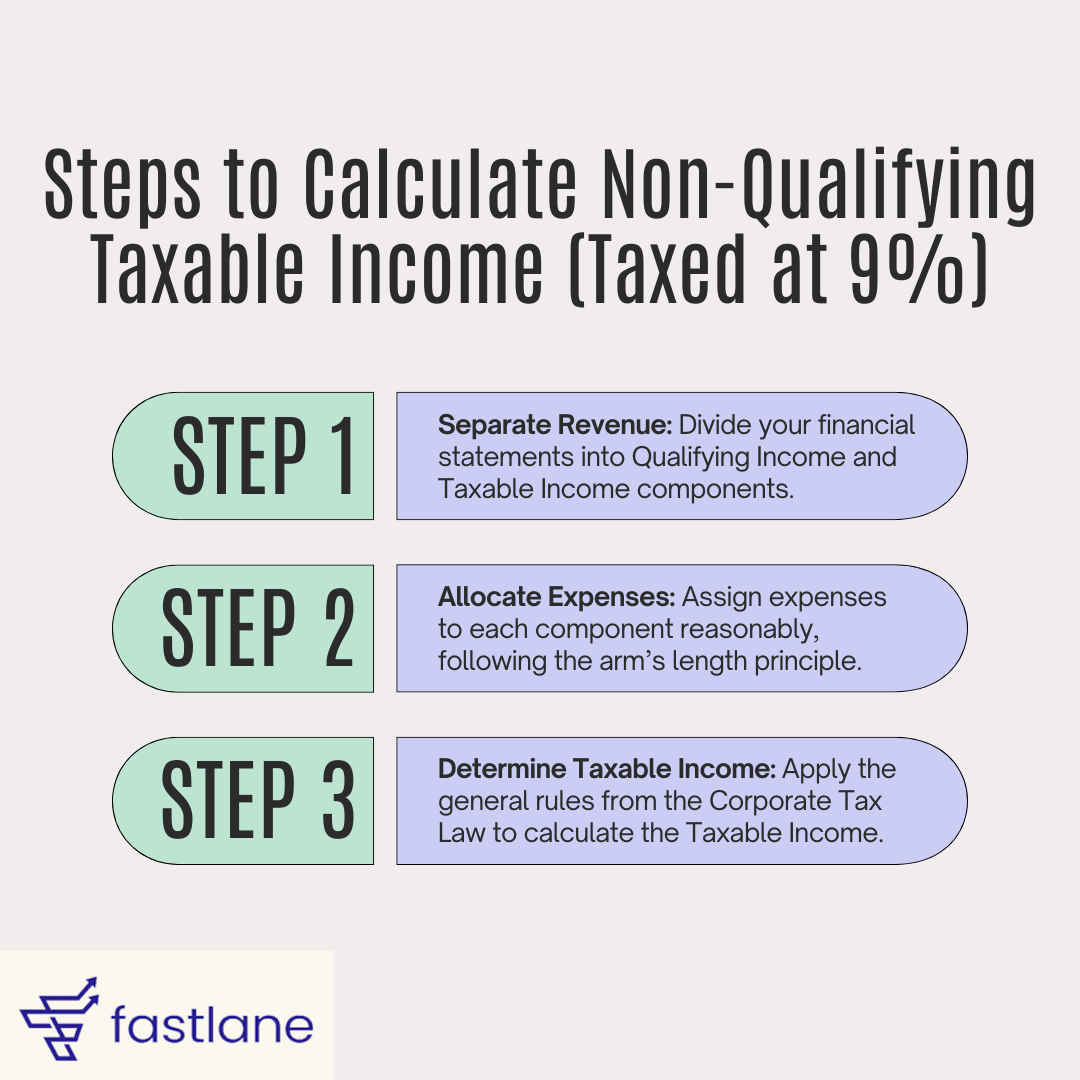

To figure out the Taxable Income that's not Qualifying Income (which is taxed at 9%), you need to:

1. Separate the revenue in your financial statements into Qualifying Income and Taxable Income components.

2. Allocate expenses against these components reasonably, following the arm’s length principle.

3. Apply the general rules for determining Taxable Income as per the Corporate Tax Law.

Let's look into a Case Study to Calculate Corporate Tax for a FreeZone Person -

Case Study 1: Tech Innovators FZE

Let's meet Tech Innovators FZE, a company in a Free Zone, UAE that deals with software development.

Here's their financial situation for the tax period ending 31 December 2024:

Revenue:

- AED 1,500,000 from Qualifying Activities within the Free Zone.

- AED 1,000,000 from activities conducted through a Domestic Permanent Establishment.

Expenses:

- AED 500,000 by the Free Zone parent.

- AED 700,000 by the Domestic Permanent Establishment.

- AED 200,000 in shared HR administrative activities, allocated equally.

Steps to Calculate Non-Qualifying Taxable Income (Taxed at 9%):

Feeling a bit overwhelmed? Don't worry, that’s where we come in. At Fastlane, we're corporate tax experts ready to help you navigate the complexities of tax compliance, including calculating corporate tax. We'll ensure you understand your obligations and help optimize your tax strategy to make the most of your Free Zone status.

So, next time you're calculating corporate tax for your Free Zone business, you'll know exactly what to do and how to benefit from the tax rules. Cheers to smart tax planning!

Created with

Login or sign up to start learningLogin to start learning