Corporate Tax is a direct tax levied on the taxable income of corporations and other businesses. It's also known as Corporate Income Tax or Business Profits Tax in other places.

In the UAE, Corporate Tax applies to companies, certain partnerships, unincorporated entities, and even natural persons conducting business activities.

Registering for corporate tax in the UAE

is crucial for compliance with the Federal Decree-Law No. 47 of 2022.

This law mandates that all taxable persons, both resident and non-resident, adhere to specific timelines for registration, ensuring transparency and proper tax administration.

Understanding these requirements helps businesses avoid penalties and align with UAE’s regulatory framework.

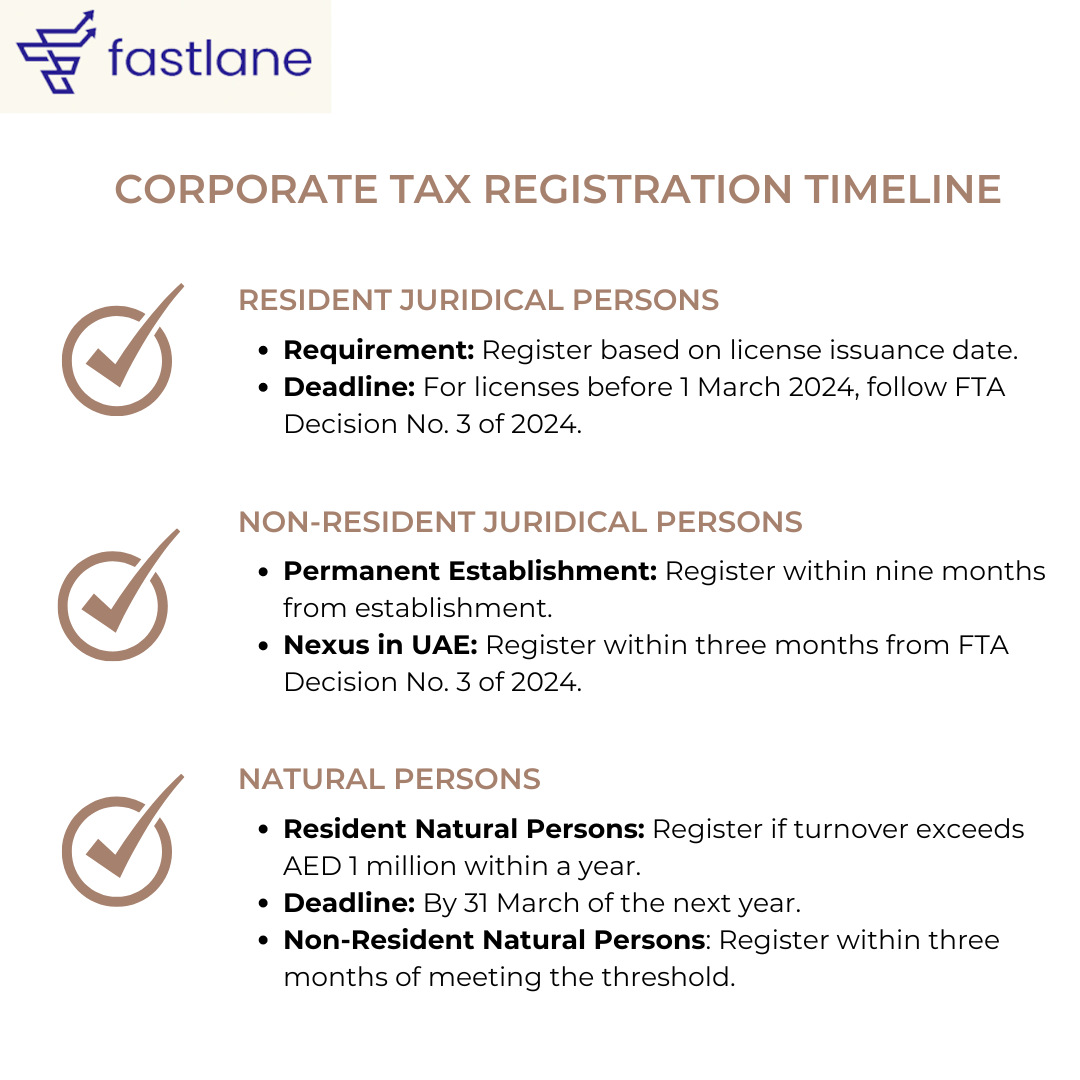

What are the Corporate Tax Registration Timelines in the UAE?

Timeline for Registration

Resident Juridical Persons:

Must register based on their license issuance date.

For licenses issued before 1 March 2024, registration deadlines are specified in FTA Decision No. 3 of 2024.

Non-Resident Juridical Persons:

If they have a permanent establishment in the UAE, they must register within nine months from its establishment date.

If they have a nexus in the UAE, they must register within three months from the effective date of FTA Decision No. 3 of 2024.

Natural Persons:

Resident natural persons must register if their business turnover exceeds AED 1 million within a calendar year, with a registration deadline by 31 March of the following year.

Non-resident natural persons with a permanent establishment must register within three months of meeting the threshold.

What are the registration deadlines for Resident Juridical Persons with licenses issued before 1 March 2024?

Juridical persons that are Resident Persons must submit a Tax Registration application for Corporate Tax based on their date of incorporation, establishment, or recognition under UAE legislation includes Free Zone and Offshore Companies.

For Entities Established Before 1 March 2024: Entities must register based on the month of their license issuance:

Registration Timeline for Resident Juridical Persons Established On or After 1 March 2024

If a juridical person is incorporated, established, or otherwise recognized in the UAE on or after 1 March 2024, they must submit a Tax Registration application within three months from the date of incorporation, establishment, or recognition.

For example, if a company is incorporated on 1 April 2024, the deadline to submit the Tax Registration application would be by 1 July 2024.

Example:

Company E

Incorporation Date: 1 April 2024

Location: Dubai, UAE

Scenario: Company E was incorporated in Dubai on 1 April 2024. As a juridical person established in the UAE on or after 1 March 2024, Company E must submit a Tax Registration application within three months from the date of incorporation.

Deadline: Company E must submit the application by 1 July 2024.

Example:

Company D

Incorporation Date: 13 August 2022

Initial Licence: Issued on 13 August 2022 to manufacture furniture (business license UAE)

Business Expansion: On 4 July 2023, Company D obtained another licence to open a retail shop for the distribution of chairs.

Scenario: Company D is a Resident Person as it was incorporated in the UAE. Since the incorporation date is before 1 March 2024, Company D must submit a Tax Registration application for Corporate Tax Registration, UAE by reference to the earliest license issuance date.

Deadline: The earliest license issuance date is 13 August 2022, so Company D must submit the application for Corporate Tax, UAE by 31 October 2024.

Example

Company G

Incorporation Date: 10 January 2023

Initial Licence: Issued on 10 January 2023 for software development.

Business Expansion: On 1 June 2023, Company G obtained another licence to offer IT consulting services.

Scenario: Company G is a Resident Person as it was incorporated in the UAE. Since the incorporation date is before 1 March 2024, Company G must submit a Corporate Tax Registration application by reference to the earliest licence issuance date.

Deadline: The earliest licence issuance date is 10 January 2023, so Company G must submit the application by 31 May 2024.

Key Takeaways

Importance of Registration: Registering for corporate tax in the UAE is mandatory under Federal Decree-Law No. 47 of 2022 to ensure compliance and proper tax administration.

2. Resident Juridical Persons: Must register for Corporate Tax, UAE based on their license issuance date, with specific deadlines for licenses issued before 1 March 2024 as per FTA Decision No. 3 of 2024.

3. Non-Resident and Natural Persons: Non-resident juridical persons with a permanent establishment have nine months to register, while those with a nexus must register within three months. Resident natural persons must register if their turnover exceeds AED 1 million within a calendar year.

- Timely Registration: Fastlane can assist businesses in adhering to the specified registration timelines, helping avoid penalties and ensuring seamless compliance with Federal Decree-Law No. 47 of 2022.

- Accurate Tax Return Filing: Fastlane handles the annual tax return preparation and filing process, ensuring timely and accurate submissions within the nine-month deadline to avoid penalties.

- Expert Compliance Support:Fastlane provides ongoing support to maintain compliance with UAE Corporate Tax regulations, including managing documentation and meeting specific conditions for exemptions.

Created with

Login or sign up to start learningLogin to start learning