Calculating Taxable Income under Corporate Tax law, UAE

This article serves as your guide, breaking down the essentials of calculating Taxable Income in a straightforward and approachable manner.

We’ll delve into what counts as exempt income, the deductions and reliefs you can claim, and how to adjust your figures to arrive at the final taxable amount.

What is Corporate Tax?

Corporate Tax is a direct tax levied on the taxable income of corporations and other businesses. It's also known as Corporate Income Tax or Business Profits Tax in other places.

In the UAE, Corporate Tax applies to companies, certain partnerships, unincorporated entities, and even natural persons conducting business activities.

How Does Corporate Tax Work?

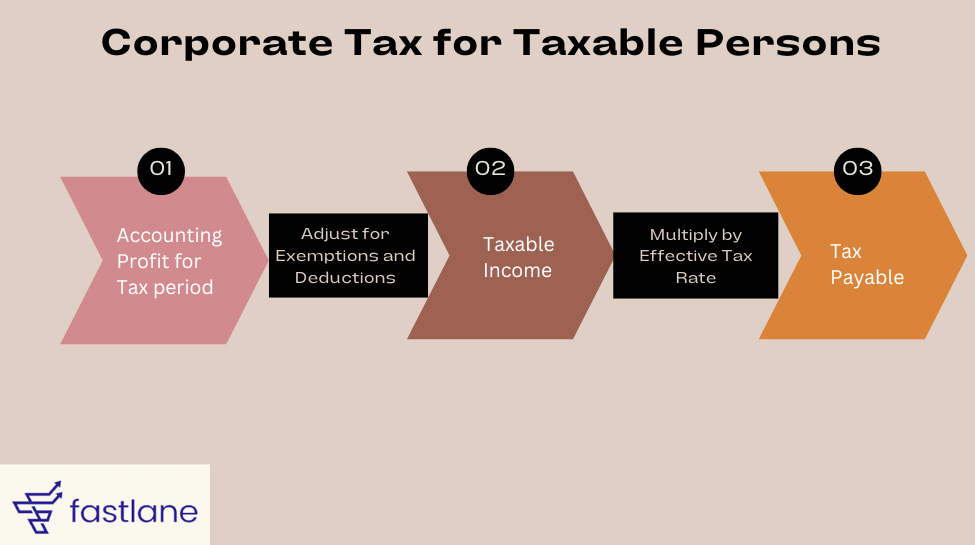

Corporate tax, UAE is calculated based on your taxable income, which is your accounting income adjusted for tax purposes.

Here's how it generally breaks down:

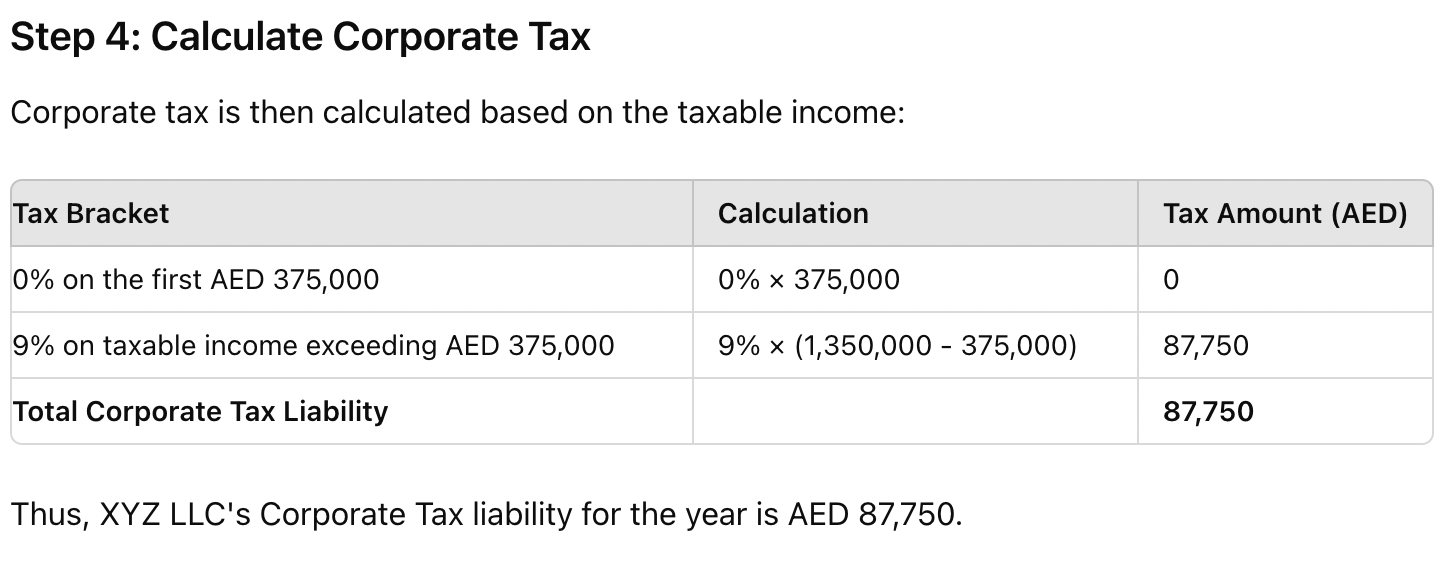

- 0% on the first AED 375,000 of taxable income.

- 9% on taxable income exceeding AED 375,000.

What is Taxable Income?

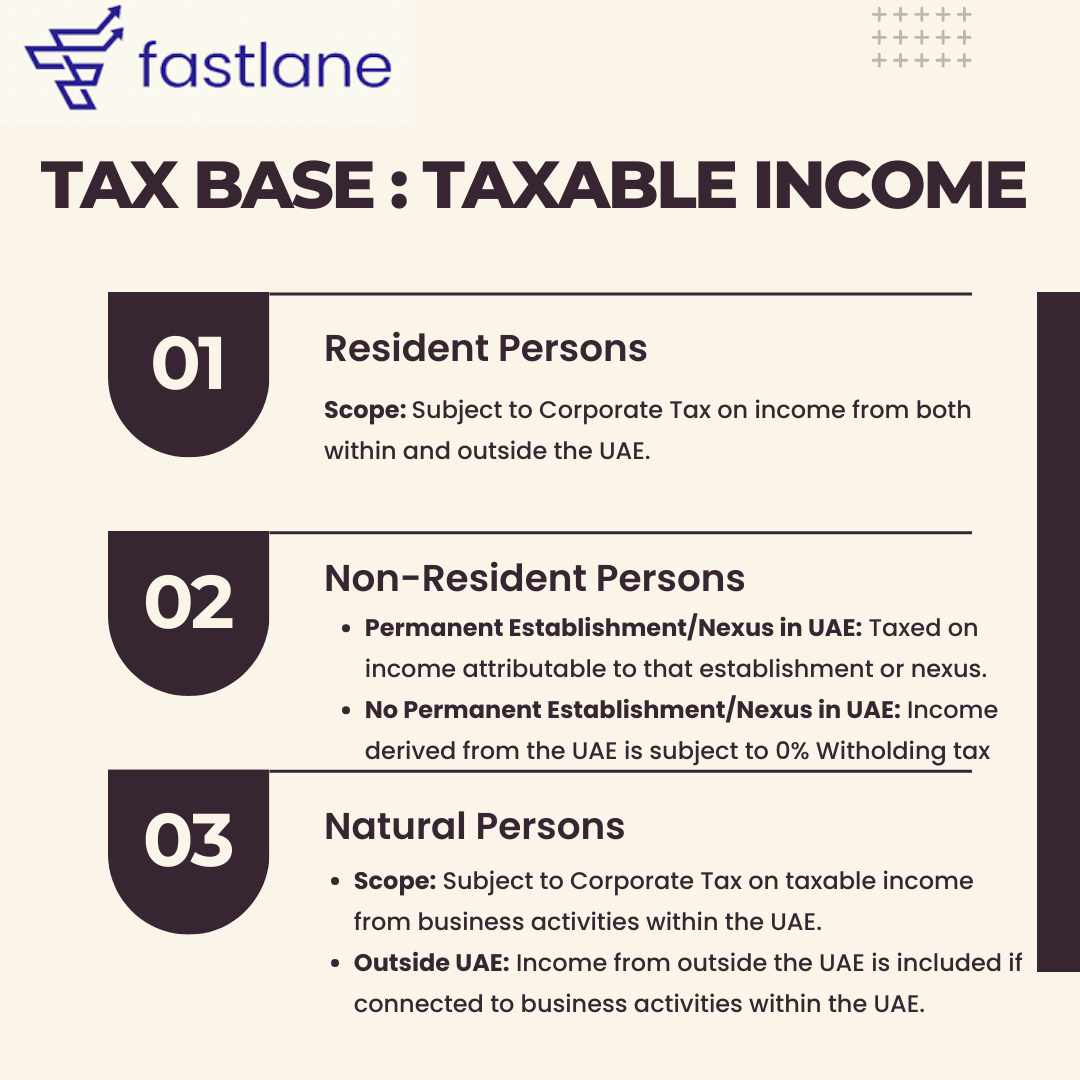

For Corporate Tax purposes, the tax base is known as a Taxable Person's Taxable Income.

Here's how it's determined:

Resident Persons: These entities are subject to Corporate Tax on their income from both within and outside the UAE. This means their global income is considered when calculating taxable income.

Non-Resident Persons: If they have a Permanent Establishment or a nexus in the UAE, they are taxed on the income attributable to that establishment or nexus. If they don't have a Permanent Establishment or a nexus but still derive income from the UAE, that income is subject to a withholding tax rate of 0%.

Natural Persons: Individuals are subject to Corporate Tax only on the taxable income from their business or business activities within the UAE. If their business activities outside the UAE are connected to those in the UAE, this income is also included.

How is the Taxable Income determined for Corporate Tax Purposes?

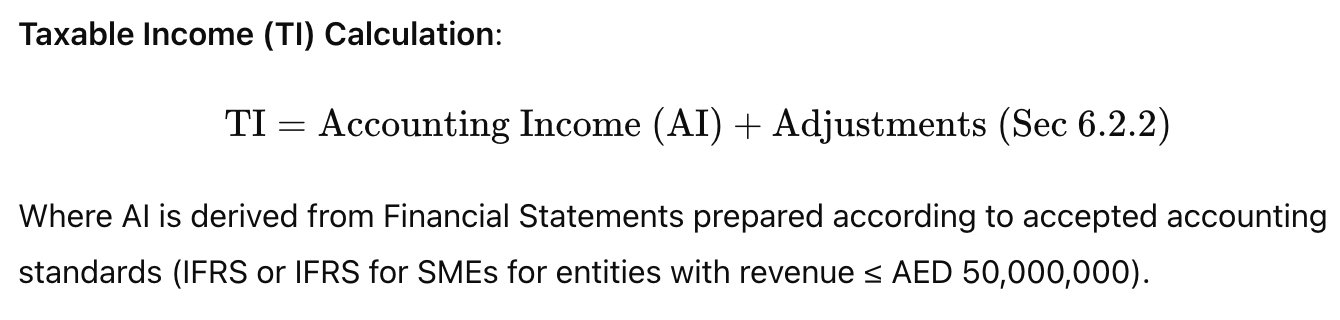

To determine taxable income, adjustments specified in Section 6.2.2 are applied to a Taxable Person's annual Accounting Income, which should be derived from Financial Statements prepared according to accepted accounting standards, such as the International Financial Reporting Standards (IFRS) or IFRS for SMEs for entities with revenue of AED 50,000,000 or less.

For businesses already maintaining accepted Financial Statements, these can be used to calculate taxable income, provided any adjustments are well-documented. This approach minimizes administrative burdens and ensures consistency.

How to adjust Accounting Income to determine Taxable Income?

When calculating Taxable Income, the following adjustments must be made to a Taxable Person's Accounting Income:

- Unrealised Gains or Losses

- Exempt Income

- Deductions

- Reliefs for Specific Transaction Types

- Transfer Pricing Adjustments (for transactions between Related Parties or Connected Persons)

- Tax Losses

Practical Example: Calculating Taxable Income for a UAE Entity

Let's consider XYZ LLC, a UAE-resident company that manufactures and sells electronics both within the UAE and internationally. Here's how XYZ LLC calculates its Corporate Tax for the year:

Step 1: Determine Accounting Income

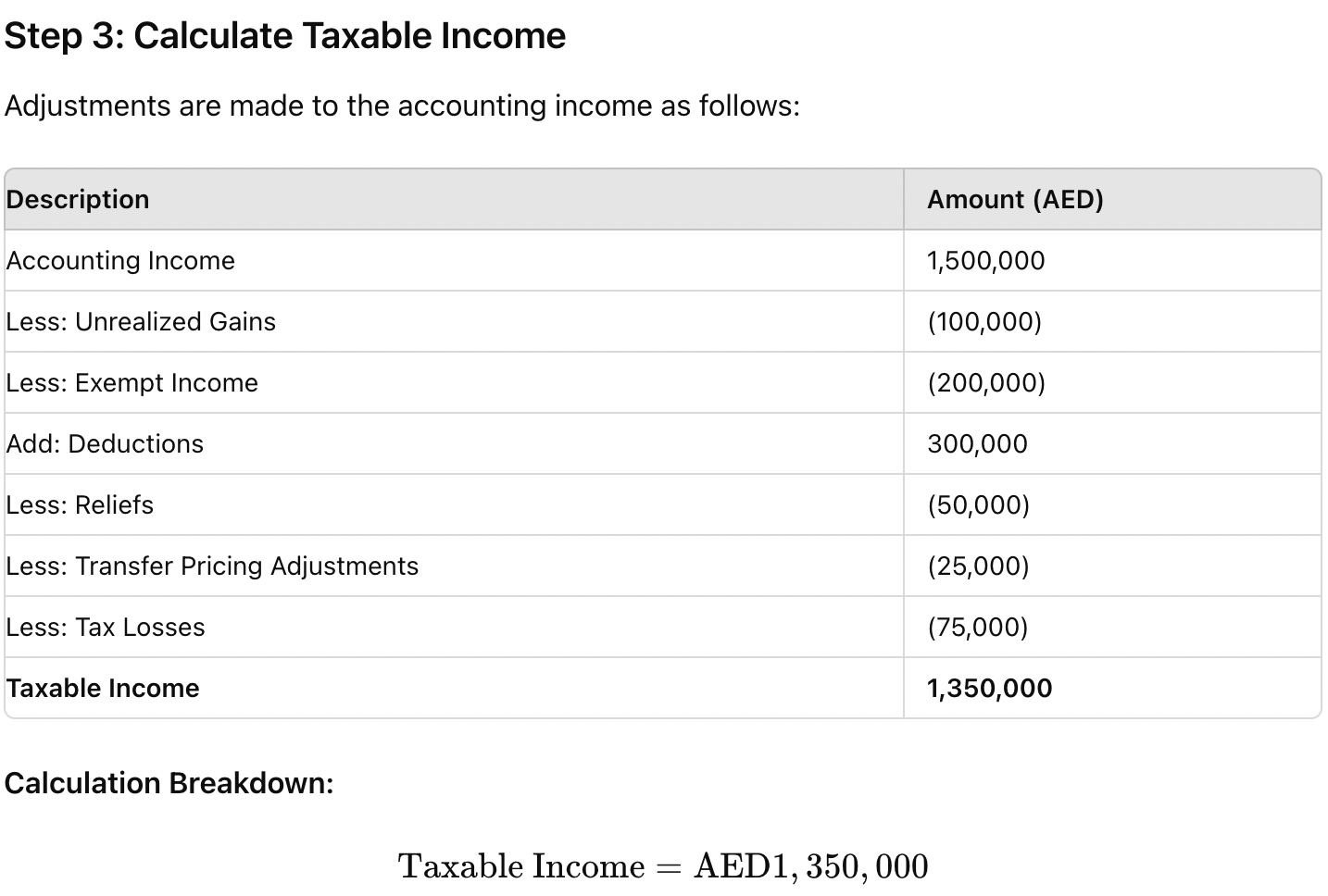

XYZ LLC's financial statements for the year, prepared according to IFRS, show an accounting income of AED 1,500,000.

Step 2: Identify Adjustments

To calculate taxable income, XYZ LLC needs to adjust its accounting income for the following:

- Unrealised Gains or Losses: XYZ LLC has unrealized gains from revaluing its assets amounting to AED 100,000. These are excluded from the taxable income.

- Exempt Income: XYZ LLC earned AED 200,000 from its foreign branches, which are already taxed abroad and exempt from UAE Corporate Tax.

- Deductions: XYZ LLC incurred deductible expenses of AED 300,000 related to its taxable income activities.

- Reliefs for Specific Transaction Types: The company availed reliefs amounting to AED 50,000 for specific qualifying transactions.

- Transfer Pricing Adjustments: XYZ LLC made a transfer pricing adjustment of AED 25,000 for transactions with related parties to comply with the arm's length principle. - Tax Losses: The company carried forward tax losses of AED 75,000 from previous years.

Key Takeaways

Understanding Taxable Income: Taxable income is derived from accounting income with specific tax adjustments applied.

2. Corporate Tax Rates: 0% on the first AED 375,000 and 9% on income exceeding AED 375,000.

3. Resident and Non-Resident Rules: Residents taxed on global income; non-residents on income related to UAE activities.

4. Necessary Adjustments: Includes unrealized gains, exempt income, deductions, and specific transaction reliefs.

- Comprehensive Tax Planning: Fastlane ensures all entities, from corporations to individuals, comply with UAE Corporate tax laws, minimizing liabilities through expert tax planning and strategic advice.

- Accurate Tax Return Filing: Fastlane handles the annual tax return preparation and filing process, ensuring timely and accurate submissions within the nine-month deadline to avoid penalties.

- Expert Compliance Support:Fastlane provides ongoing support to maintain compliance with UAE Corporate Tax regulations, including managing documentation and meeting specific conditions for exemptions.

Created with

Login or sign up to start learningLogin to start learning