What are Investment funds and Investment managers?

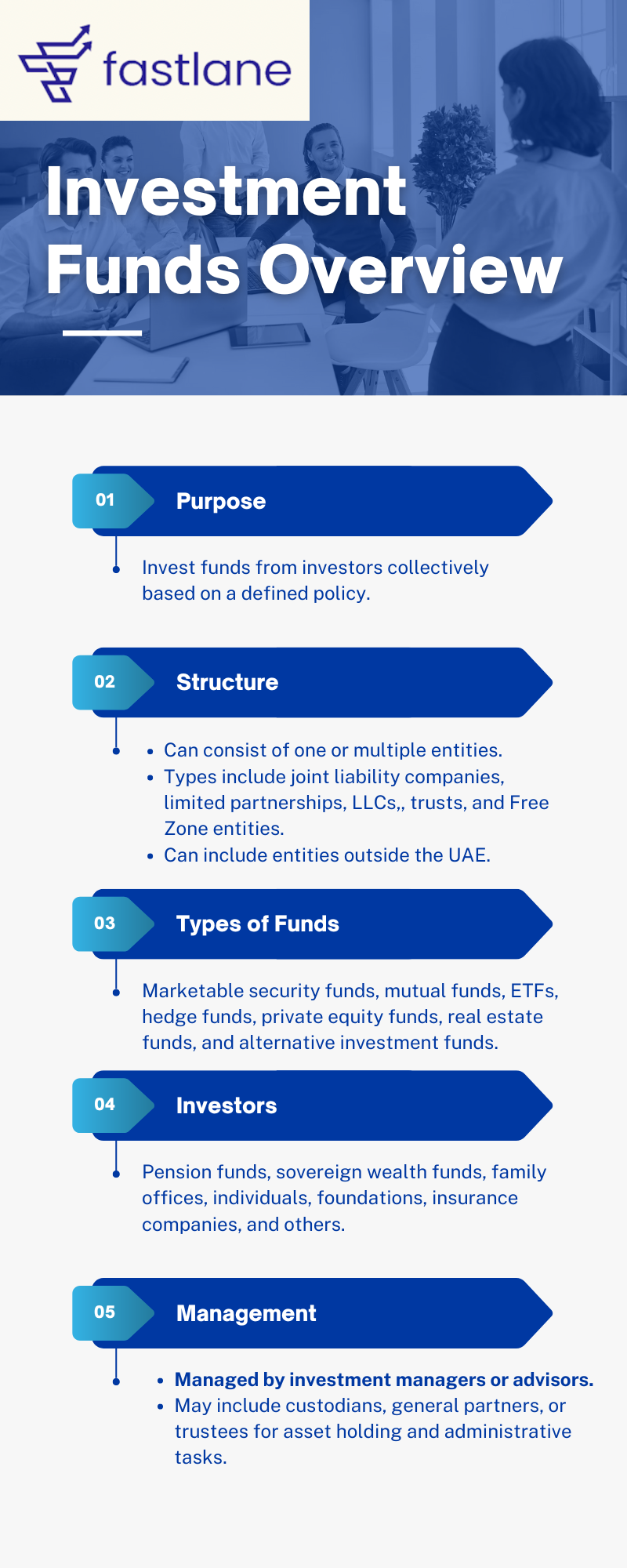

Investment funds pool funds from investors to invest collectively based on a defined investment policy, allowing investors to share in the profits. These funds can include various entities and operate in different forms, such as companies or partnerships, and may be based in the UAE or abroad. Common types of investment funds include mutual funds, hedge funds, and real estate funds.

Key Points 1. Structure and Types: Investment funds can be joint liability companies, limited partnerships, LLCs, public/private joint stock companies, or trusts. Common fund types: marketable security funds, mutual funds, ETFs, money-market funds, hedge funds, private equity funds, real estate funds, and alternative investment funds.

2. Investors and Capital: Investors, including pension funds, sovereign wealth funds, family offices, and individuals, provide capital for returns. The fund uses this capital for investments and business activities to generate profits.

3. Management: Funds may appoint Investment managers to make decisions per a pre-agreed policy. Managers or advisors might subcontract tasks to sub-advisors. Custodians or trustees may hold assets or perform administrative tasks.

4. Income and Fees: Investment managers earn through management fees, performance fees, or co-investments.

Fees are based on capital committed, invested, or assets managed, and can include a share of excess returns.

Overview of Investment Funds in the UAE

The UAE's investment funds landscape offers a wide range of financial products similar to those available in global markets, including public and private funds. Key Points

Public vs. Private Funds:

Public funds are available to the general public, while private funds are restricted to professional investors.

Variety of Investment Strategies:

Investment funds in the UAE can include private equity, venture capital, real estate, money market, crypto tokens, hedge funds, and Islamic funds, each with unique investment strategies and focuses.

What is the Corporate Tax treatment of Investment Funds?

The Corporate Tax treatment of investment funds in the UAE varies depending on whether they are Resident Persons, Unincorporated Partnerships, or Non-Resident Funds.

Here's a breakdown of the treatment for each category.

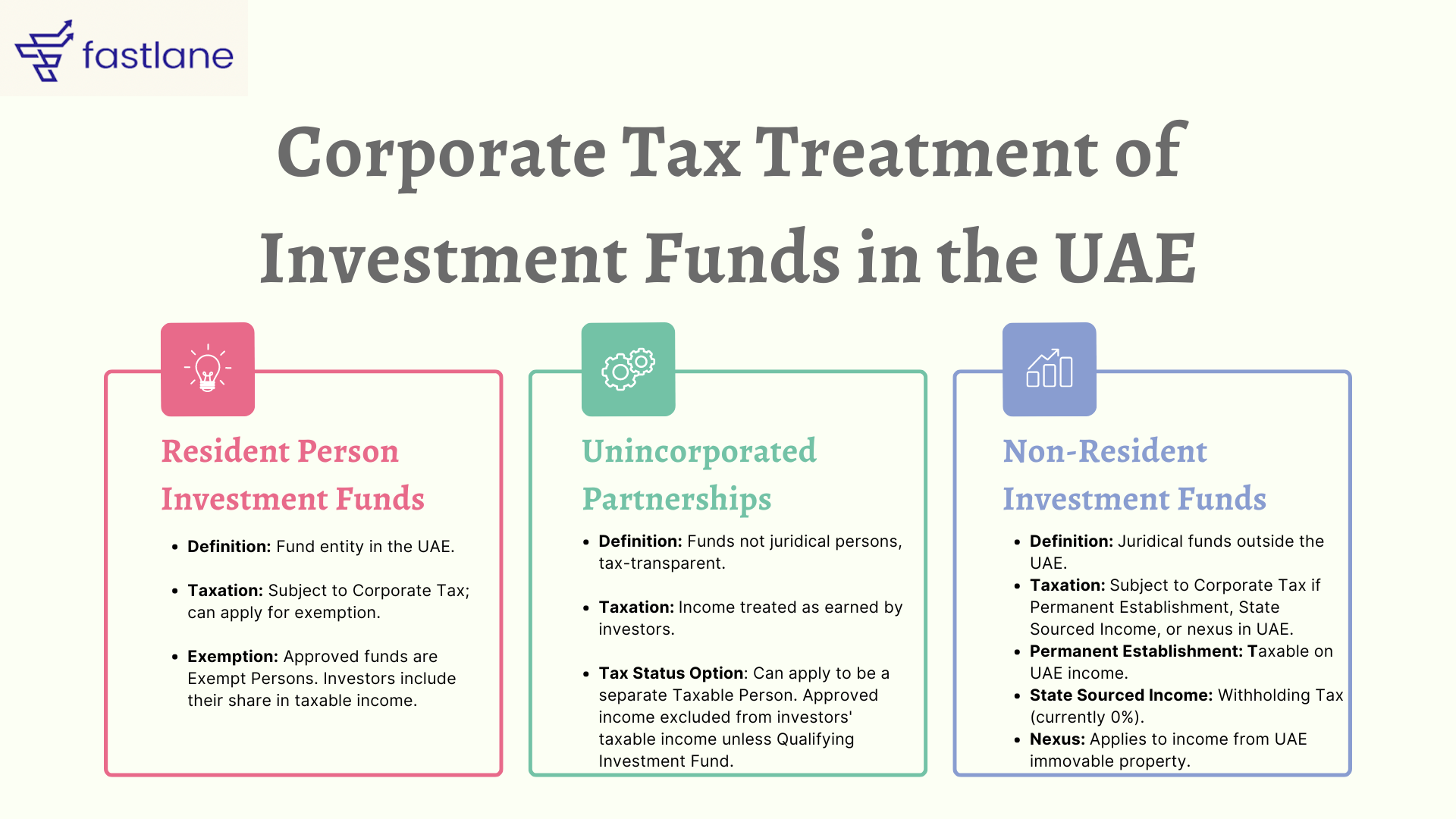

1. Resident Person Investment Funds

- Definition: Any entity that is part of a fund structure and is a juridical person, incorporated in the UAE or managed and controlled in the UAE.

- Taxation: Subject to Corporate Tax but can apply for exemption as a Qualifying Investment Fund if conditions are met.

- Exemption: If approved, the fund becomes an Exempt Person and not subject to Corporate Tax. Investors include their proportional share of the fund's income in their taxable income.

2. Unincorporated Partnerships

- Definition: Investment funds established as Unincorporated Partnerships are not considered juridical persons and are transparent for tax purposes.

- Taxation: Income is treated as earned by the investors for Corporate Tax purposes.

- Option for Tax Status: Investors can apply for the partnership to be treated as a separate Taxable Person (fiscally opaque). If approved, the partnership's income is not included in the investors' taxable income unless it becomes a Qualifying Investment Fund.

3. Non-Resident Investment Funds

- Definition: Investment funds established as juridical persons outside the UAE and not managed and controlled within the UAE.

- Taxation: Subject to Corporate Tax if they have a Permanent Establishment, State Sourced Income, or a nexus in the UAE.

- Permanent Establishment: Taxable on income attributable to the UAE establishment.

- State Sourced Income: May be subject to Withholding Tax, but currently set at 0%.

- Nexus: Applies to non-resident juridical persons earning income from immovable property in the UAE.

Taxation of Investment managers' fees

Investment managers' fees for brokerage or investment services are subject to UAE Corporate Tax if they are Resident Persons.

Non-Resident investment managers may also be taxed if they have a Permanent Establishment in the UAE or earn State Sourced Income, though the current Withholding Tax rate is 0%.

Key Takeaways

1. Diverse Structures and Types: Investment funds can take various forms, including companies, partnerships, and trusts. They can be based in the UAE or abroad, with common types such as mutual funds, hedge funds, and real estate funds.

2. Investor Roles and Capital: Investors, including pension funds and individuals, provide capital to investment funds, which use this capital to generate returns through various business activities.

3. Taxation of Funds and Managers:

- Resident Investment Funds: Subject to Corporate Tax but may be exempt if they qualify as a Qualifying Investment Fund.

- Unincorporated Partnerships: Income is taxed at the investor level.

- Non-Resident Funds: Taxed if they have a Permanent Establishment, State Sourced Income, or nexus in the UAE.

- Investment Managers: Fees earned are subject to Corporate Tax if they are Resident Persons or have a Permanent Establishment in the UAE.

1. Comprehensive Corporate Tax Guidance: - Fastlane provides tailored tax advice to ensure your investment fund benefits from available exemptions and favorable tax treatments

2. Ministry of Finance Notifications: - Assist with the preparation and submission of notifications to the Ministry of Finance in the required form and manner. - Ensure that your business meets all the notification requirements to maintain tax exemption status.

3. Ongoing Compliance and Advisory:

- Provide regular updates and advisory on changes in the Corporate Tax Law and how they impact your business.

Created with

Login or sign up to start learningLogin to start learning