Corporate Tax for a business with Both Extractive and other activities

A business might be engaged in both extractive or non-extractive activities and other types of business. How is the taxable income determined in that case?

How is Taxable Income determined for a business with both Extractive and other activities?

The Taxable Income for a business with both Extractive/Non-Extractive Natural Resource activities and other activities is determined by

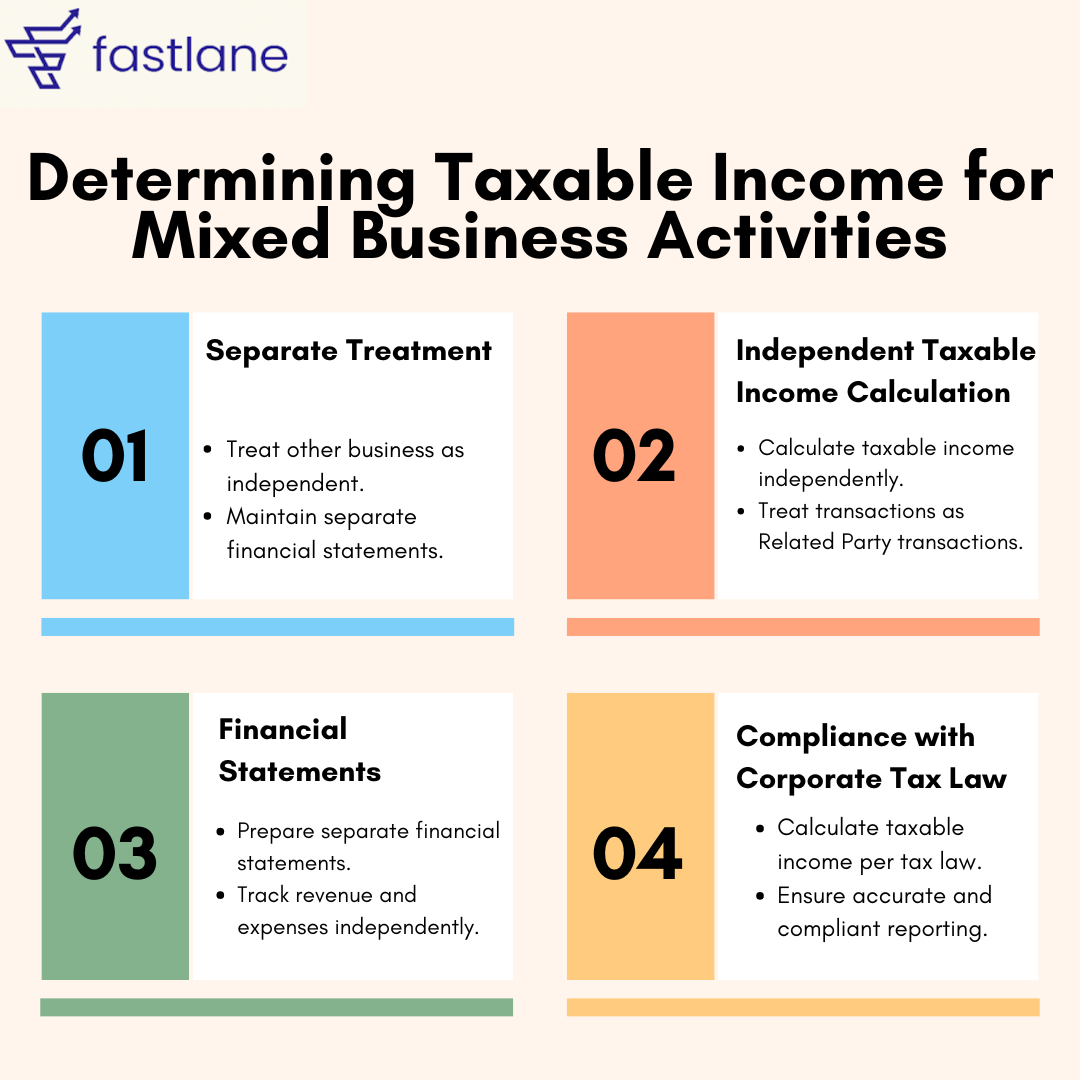

treating the other business as a separate entity ("Separate Entity Approach").This involves maintaining separate financial statements and calculating Taxable Income independently according to Corporate Tax Law provisions.

Key Points

- The other business is treated as a separate entity with its own independent financial statements.

- Taxable Income for the other business is calculated independently, based on its financial performance.

- Transactions between the businesses are considered Related Party transactions and must adhere to specific guidelines.

- Compliance with Corporate Tax Law is ensured by accurately calculating and reporting Taxable Income for each business separately.

Step-by-Step Activities for Determining Taxable Income from Other business

- Step-1 Identify and Separate Businesses : Determine the scope of both the Extractive/Non-Extractive Natural Resource Business and the other business. Establish separate processes and systems for each business to ensure they operate independently.

- Step-2. Maintain Independent Financial Statement: Set up distinct accounting systems for each business. Record all financial transactions separately to ensure clear differentiation between the businesses.

- Step-3. Calculate Independent Taxable Income: Calculate revenue and expenses for the other business independently. Determine Taxable Income based on the financial performance of the other business, adhering to the Corporate Tax Law provisions.

- Step-4. Manage Related Party Transactions: Identify and document any transactions between the businesses. Ensure these transactions comply with the arm’s length principle and are accurately recorded as Related Party transactions.

- Step-5. Ensure Compliance with Corporate Tax Law: Review relevant tax provisions. Verify the accuracy of Taxable Income calculations and maintain thorough documentation to demonstrate compliance during audits.

Practical Example

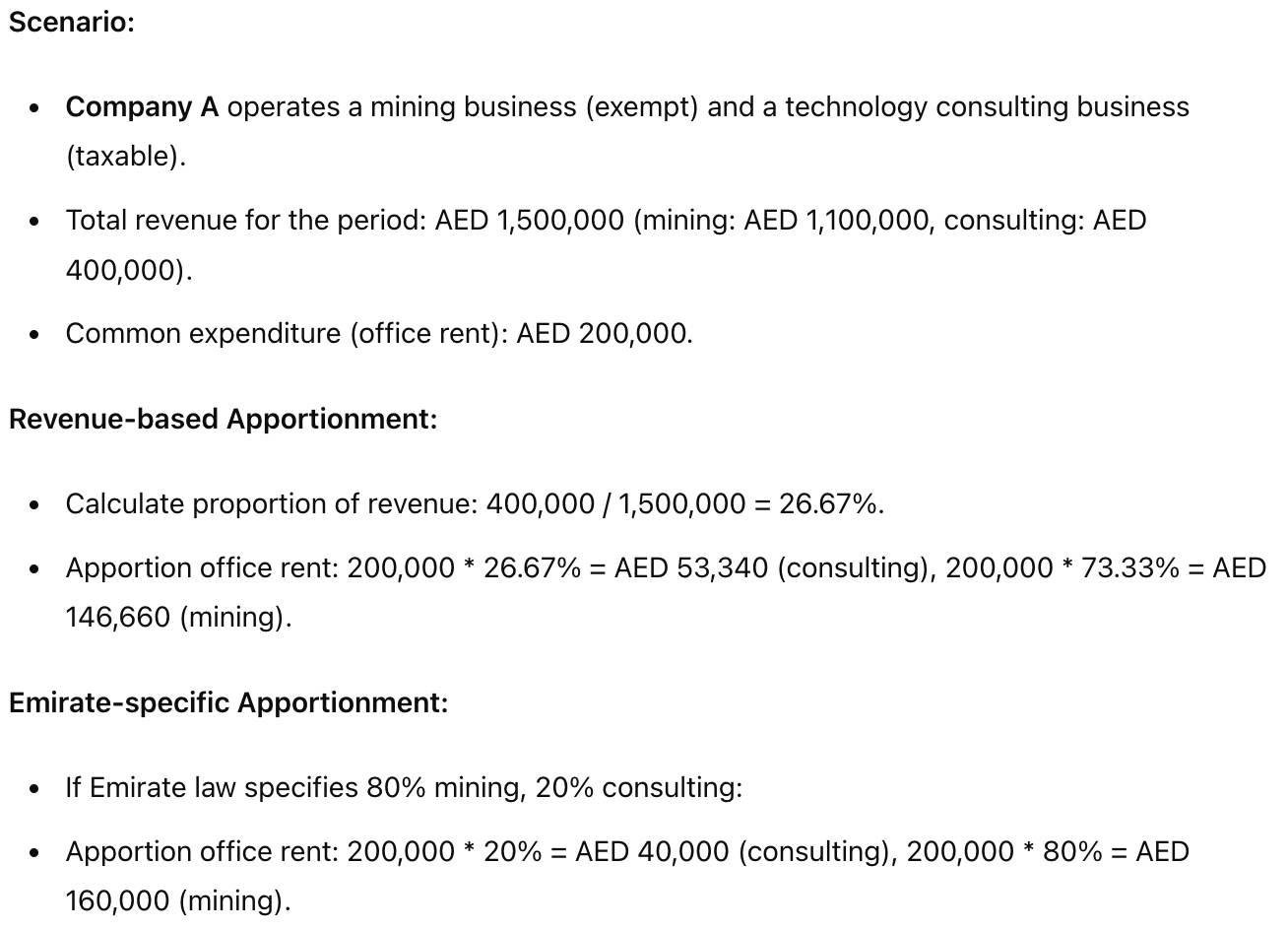

Example 1: Mining and Consulting Business

Application:

Example 2: Oil Extraction and Retail Business

Application:

Apportionment of Expenditure

When a business operates both Extractive/Non-Extractive Natural Resource activities and other taxable activities, expenses must be properly attributed. This can involve direct attribution for specific expenses and appropriate apportionment methods for common expenditures.

Practical Example - Expense Apportionment

Compliance Requirements

1. Record Keeping

- Maintain all records and documents to verify exemption status for 7 years after the tax period.

2. Tax Registration

- Exempt Persons are not required to register for Corporate Tax unless conducting a taxable business.

- If conducting taxable business, registration with the FTA is required.

- Deregistration is possible if the taxable business ceases.

- Businesses with revenue exceeding 5% of total revenue must remain registered even if falling below the threshold later, filing a nil Tax Return if applicable.

3. Applicable Accounting Standards

- Maintain separate Financial Statements for the taxable business.

- Prepare Financial Statements based on IFRS or IFRS for SMEs if revenue does not exceed AED 50 million.

4. Preparing Audited Financial Statements

- Prepare and maintain Financial Statements for the taxable business.

- Audit Financial Statements if the taxable business's revenue exceeds AED 50 million or if it is a Qualifying Free Zone Person.

5. Tax Return

- File a Tax Return for the taxable business within 9 months from the end of the relevant tax period, in the prescribed form and manner.

Key Takeaways

How Fastlane can help?

Fastlane Consultancy can assist businesses in navigating the complexities of compliance by ensuring accurate financial segregation, and providing guidance on maintaining compliance with Corporate Tax Law.

We offer expertise in preparing independent financial statements and managing related party transactions to ensure accurate and compliant taxable income calculations.

Get In Touch

Location

Phone Number

+971-551273479