Exempt Persons: Who don’t have to pay Corporate Tax in UAE?

Certain individuals and entities are granted exemptions from Corporate Tax due to compelling public interest and policy reasons, ensuring they are not subject to taxation.

These entities are referred to as "Exempt Persons."

These entities are referred to as "Exempt Persons."

Who Qualifies as an Exempt Person Under UAE Corporate Tax Law?

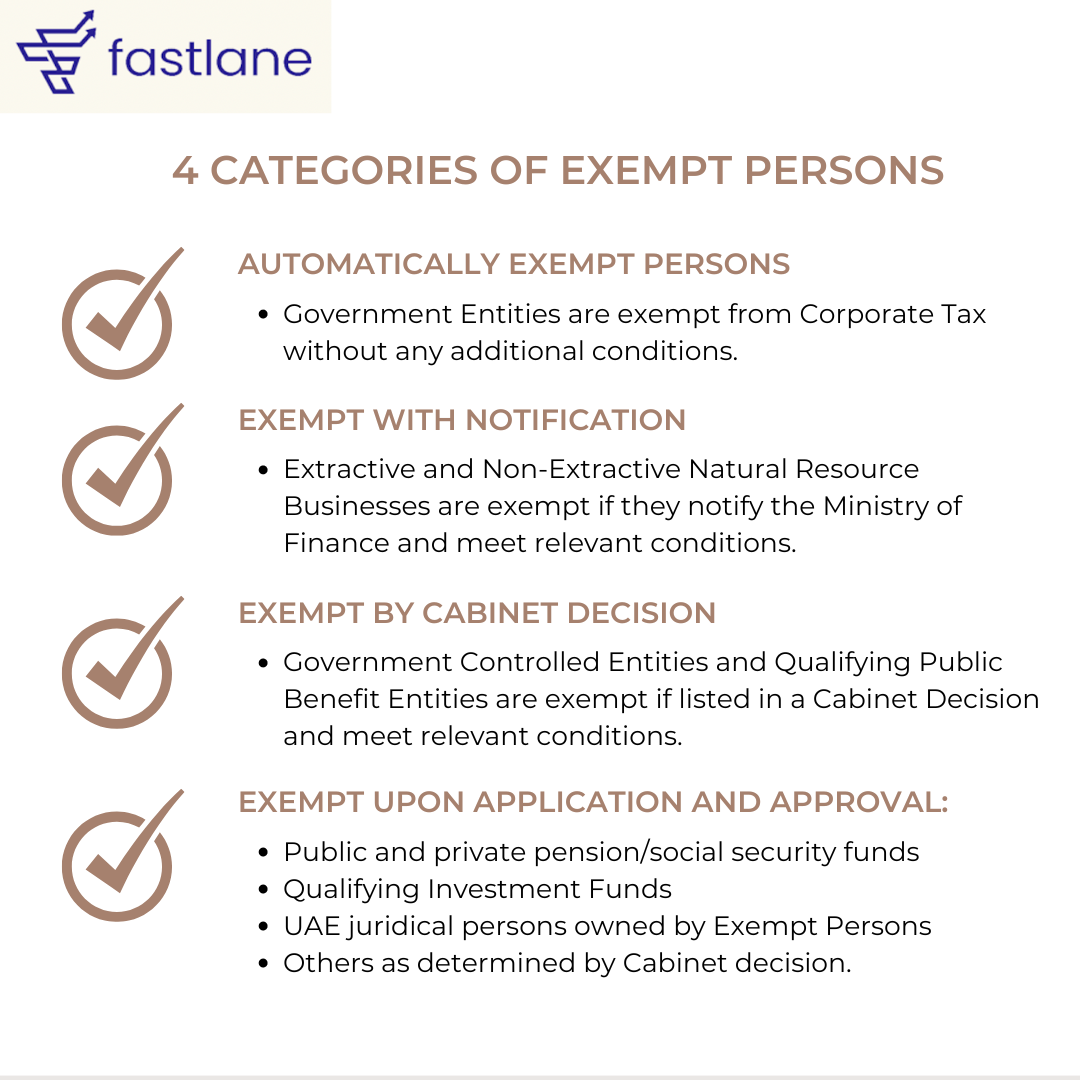

Exempt Persons fall into one of four categories:

1. Automatically Exempt Persons:

- Government Entities are exempt from Corporate Tax without any additional conditions.

2. Exempt with Notification:

- Extractive Businesses and Non-Extractive Natural Resource Businesses are exempt if they notify the Ministry of Finance and meet relevant conditions.

- Extractive Businesses and Non-Extractive Natural Resource Businesses are exempt if they notify the Ministry of Finance and meet relevant conditions.

3. Exempt by Cabinet Decision:

- Government Controlled Entities and Qualifying Public Benefit Entities are exempt if listed in a Cabinet Decision and meet relevant conditions.

4. Exempt upon Application and Approval:

- Public and private pension or social security funds

- Qualifying Investment Funds

- Juridical persons in the UAE wholly owned and controlled by certain Exempt Persons

- Any other Person determined by a Cabinet decision at the suggestion of the Minister.

Hey there!

Let's dive into the world of corporate tax exemptions. It’s like getting a golden ticket for your business, and understanding who qualifies can save you a lot of money. So, grab a coffee, and let’s break it down.

Let's dive into the world of corporate tax exemptions. It’s like getting a golden ticket for your business, and understanding who qualifies can save you a lot of money. So, grab a coffee, and let’s break it down.

What are Exempt Persons?

Exempt Persons are entities that don’t have to pay corporate tax because there are strong public interest and policy reasons for their exemption. These exemptions can make a big difference for certain types of organizations.

Categories of Exempt Persons

Exempt Persons fall into four main categories:

1. Automatically Exempt Persons: Government Entities.

2. Exempt with Notification: Extractive Businesses and Non-Extractive Natural Resource Businesses.

3. Exempt with Cabinet Decision: Government Controlled Entities and Qualifying Public Benefit Entities.

4. Exempt with FTA Approval: Public and private pension funds, Qualifying Investment Funds, certain juridical persons, and others as determined by the Cabinet.

1. Automatically Exempt Persons

This category includes Government Entities like federal and local government departments, agencies, and authorities. These entities are considered exempt automatically because they perform governmental and public duties. However, if they conduct business under a license, they are taxed on that specific business activity.

Example: The Ministry of Education is automatically exempt, but if it sets up a bookstore, that bookstore’s profits might be subject to corporate tax.

2. Exempt with Notification

Extractive Businesses (like oil and gas companies) and Non-Extractive Natural Resource Businesses (like processing raw materials) can be exempt if they notify the Ministry of Finance and meet certain conditions. They must be subject to Emirate-level taxation and operate under a government license.

Example: A mining company extracting gold must notify the Ministry to be exempt from corporate tax, provided it meets the relevant conditions.

3. Exempt with Cabinet Decision

Government Controlled Entities and Qualifying Public Benefit Entities can be exempt if listed in a Cabinet Decision. These entities must be wholly owned and controlled by a government entity and operate for public benefit purposes like education, health, or cultural activities.

Example: A public university funded by the government can be exempt from corporate tax if it is listed in the Cabinet Decision and operates exclusively for educational purposes.

4. Exempt with FTA Approval

Entities like public and private pension funds, Qualifying Investment Funds, and certain juridical persons can apply to the Federal Tax Authority (FTA) for exemption. They need to meet specific conditions and demonstrate their eligibility for the exemption.

Example: A private pension fund providing retirement benefits to employees can apply to the FTA for exemption from corporate tax, ensuring it meets all regulatory conditions.

Practical Case Study: Company X

Scenario: Company X is a Qualifying Investment Fund.

Category: Exempt with FTA Approval.

Steps:

1. Apply to the FTA demonstrating compliance with regulatory oversight.

2. Ensure its interests are traded on a recognized stock exchange or widely available to investors.

3. Prove its primary purpose is not to avoid corporate tax.

By following these steps, Company X can gain exemption status and avoid paying corporate tax.

Why It Matters

Understanding these exemptions is crucial for planning your business finances and ensuring compliance with tax laws. It can significantly reduce your tax burden and free up resources for other important business activities.

Need Help?

Navigating the world of tax exemptions can be tricky. Fastlane is here to help. We’re experts in corporate tax and can guide you through the process, ensuring your business gets the exemptions it deserves.

Get In Touch

Location

Fastlane Management Consultancy, Office No 33, 2nd Floor, Sheikh Rashid Building, Al Souq Street, Bur Dubai, Dubai

Phone Number

+971-551273479

Phone Number

+971-551273479

Created with