Impact of Small Business Relief on other Corporate Tax rules

What is Small Business Relief?

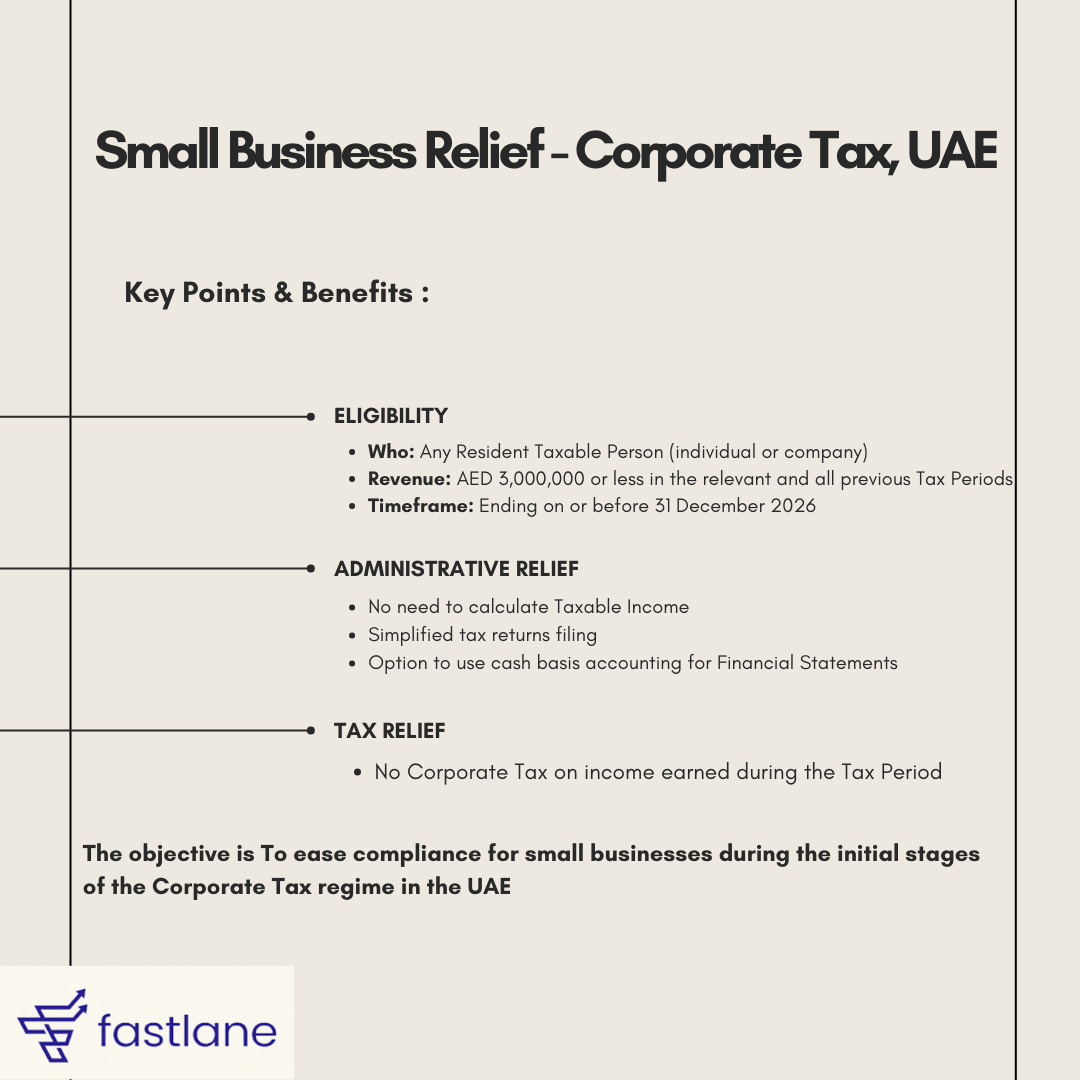

Small Business Relief is a measure to help small businesses in the UAE manage the Corporate Tax system more easily. It reduces the compliance burden by simplifying tax obligations for eligible businesses.

Key Points: - Eligibility : Any Resident Taxable Person (individual or company) with revenue of AED 3,000,000 or less in the relevant and all previous Tax Periods ending on or before 31 December 2026. Benefits:

Administrative Relief: Eligible businesses don’t need to calculate their Taxable Income and can file simplified tax returns. They can also use cash basis accounting for their Financial Statements.

Tax Relief: No Corporate Tax is required to be paid on income earned during the Tax Period.

This relief aims to make it easier for small businesses to comply with tax regulations during the early stages of the Corporate Tax regime.

Impact of Small Business Relief on other Corporate Tax rules, including tax losses, interest deduction limitations

Tax Losses

When a business elects for Small Business Relief, it cannot accrue, utilize, or transfer tax losses for that tax period.

Unutilized tax losses from previous periods can be carried forward to future periods when the relief is not elected.

Example: ABC LLC had a tax loss of AED 400,000 from a previous period. If ABC LLC elects for Small Business Relief in the current period, it cannot use the AED 400,000 loss this year but can carry it forward to future periods.

General Interest Deduction Limitation Rule

Overview of General Interest Deduction Limitation Rule

The general interest deduction limitation rule allows businesses to deduct net interest expenditure up to 30% of their EBITDA (earnings before interest, tax, depreciation, and amortization).

This limitation applies only if net interest expenditure exceeds AED 12,000,000 for the tax period. Excess interest expenditure beyond this limit cannot be deducted in the current period but can be carried forward for up to ten tax periods.

Impact of Electing for Small Business Relief

If a business opts for Small Business Relief, the general interest deduction limitation rule does not apply.

This means the business cannot carry forward any net interest expenditure incurred during that tax period.

Additionally, any previously carried forward net interest expenditure cannot be utilized in the relief period but can be used in future periods when Small Business Relief is not elected.

Exempt Income and Small Business Relief

Exempt Income includes specific types of income that are not taxable under Corporate Tax Law. This encompasses dividends and profit distributions from UAE-resident juridical persons, income from participating interests, and income from foreign permanent establishments, provided certain conditions are met. Impact of Electing for Small Business Relief:

When a business elects for Small Business Relief, the rules for Exempt Income do not apply.

This means that all income, including normally exempt income, must be included when calculating revenue to determine eligibility for Small Business Relief.

Compliance and Record-Keeping for Small Business Relief

Requirement to Self-Assess, Register, and Make an Election:

To claim Small Business Relief, an eligible Taxable Person must register for Corporate Tax and elect for the relief by filing a Tax Return each Taxable Period.

Requirement to File Tax Returns:

Businesses must make the election for Small Business Relief within their Tax Returns. The relief allows for a simplified Tax Return, reducing the required information and time needed for completion.

Records Required to Demonstrate Revenue:

Businesses must maintain records and documentation to support the information in their Tax Return and to demonstrate that their revenue did not exceed the Small Business Relief threshold of AED 3,000,000 for the relevant and previous Tax Periods.

Records include bank statements, sales ledgers, invoices, order records, delivery notes, and other relevant correspondence.

Record-Keeping Period:

All records and documents must be kept for seven years following the end of the Tax Period they relate to, not the period they were created. This ensures that records are available for FTA inspection if required.

Fastlane: Your Corporate Tax Partner : Fastlane provides expert guidance to ensure your business meets the eligibility criteria for Small Business Relief, assists in streamlined tax filing, and offers comprehensive compliance support to help you navigate the Corporate Tax system in the UAE.

Created with

Login or sign up to start learningLogin to start learning