Cryptocurrency is no longer just a speculative asset — it’s now a legitimate medium of payment in the UAE, especially among tech, consulting, and Web3 firms.

But here’s the challenge: the UAE’s regulatory and tax ecosystem for virtual assets is unique — it combines VARA Rulebooks, FTA’s VATP040 clarification, and IFRS standards like IAS 38 and IFRS 15.

So how should a business — whether a crypto exchange, custodian, or even a non-crypto company that accepts Bitcoin payments — record, report, and tax these transactions properly?

Under the IFRS Interpretations Committee’s 2019 guidance, crypto can fall into two buckets:

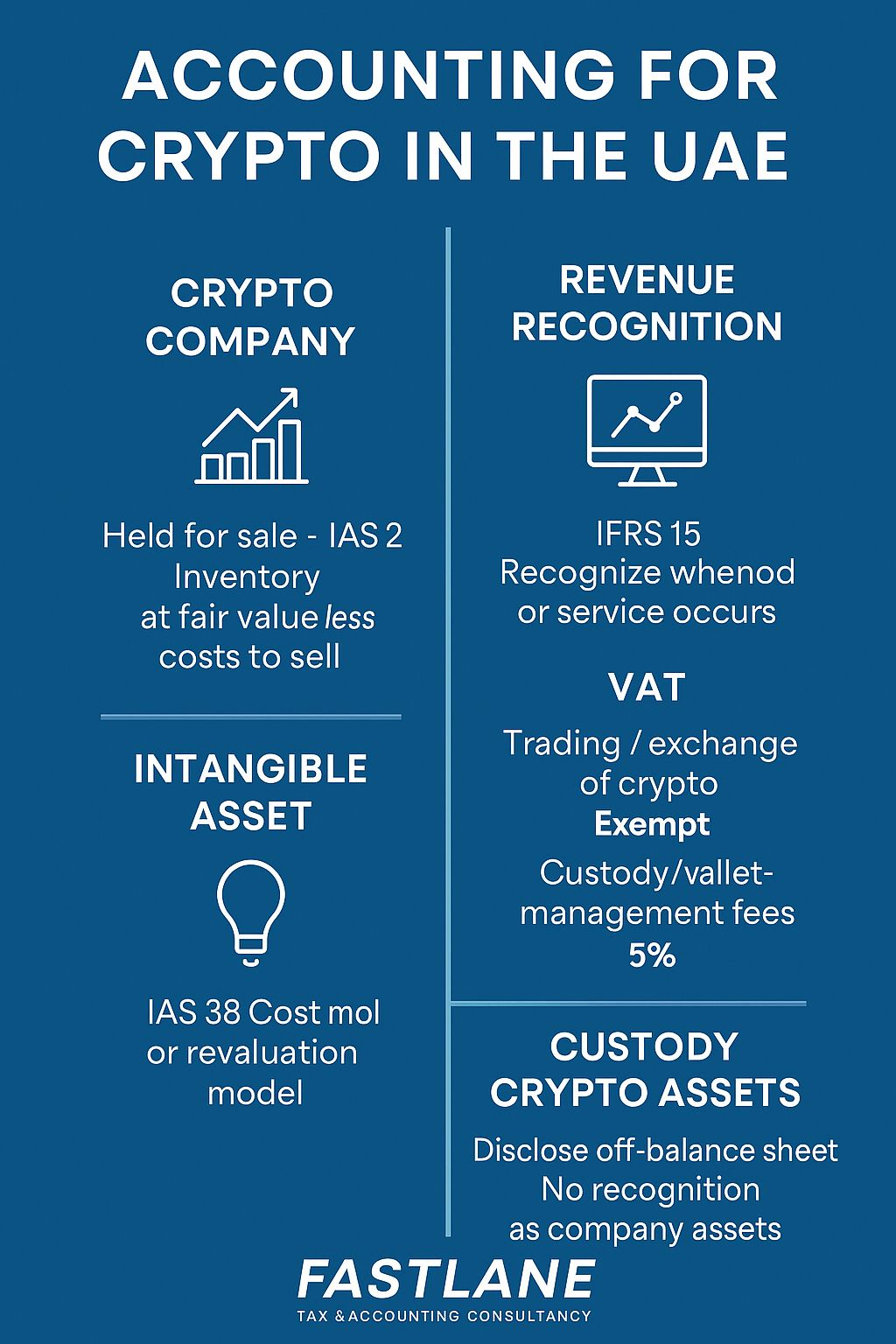

- Held for resale (brokers, exchanges) → IAS 2 – Inventories (Fair value – costs to sell through P&L)

- Held for investment or long-term use → IAS 38 – Intangible Assets (Cost or revaluation model)

Example: A UAE-licensed VARA exchange holds ETH to provide liquidity → treat as inventory (IAS 2).

A consultancy accepts BTC for fees and holds it → treat as intangible asset (IAS 38).

2. Measurement & Revaluation – Cost vs. Market Value

Under IAS 38, companies can use:

- Cost model: record at cost, test for impairment if market falls.

- Revaluation model: allowed only if there’s an active market (e.g., BTC, ETH). Gains go to OCI, losses to P&L.

Example: Fastlane Tech DMCC receives 1 BTC worth AED 250,000 in August 2025. By December 2025, BTC = AED 280,000 → revaluation gain AED 30,000 → recorded in OCI.

a) Crypto Companies

- Trading-fee revenue → recognise when trade executes.

- Custody fees → recognise over time.

VAT:

- Trading/exchange of crypto = VAT-exempt.

- Custody or wallet services = 5% VAT (if supplier in UAE).

b) Non-Crypto Businesses Paid in Crypto

Even if your service is EOR, consulting, or marketing:

- Revenue recognised at fair value of crypto (AED equivalent) on transaction date.

- VAT at 5% of AED value, even if you’re paid in BTC or USDT.

- Tax invoice must be issued in AED.

Under VARA rules, client assets remain client property. Therefore:

- Do not recognise client crypto on your balance sheet.

- Disclose total value in the notes (“Assets held for clients”).

- Only recognise custody fees as revenue.

This mirrors IFRS’s “no control, no recognition” principle.

If crypto received for services is later sold at a higher price:

- The increase is Other Income (fair-value gain), not service revenue.

- Under UAE Corporate Tax, that gain is taxable, as it appears in your P&L.

Example: 0.05 BTC received at AED 12,500 → sold later for AED 14,000 → AED 1,500 gain → taxable under 9% CT.

Paying suppliers in crypto = disposal of an intangible asset.

If the crypto’s market value differs from book value:

- Record gain or loss in P&L.

- VAT applies to your underlying supply (not the crypto).

- For CT, any realised gain/loss is part of taxable income.

Framework | Focus | What It Means for You

VARA Rulebook | Licensing, custody, marketing conduct | Define scope of activity & ensure AML/KYC readiness

FTA VATP040 | VAT treatment of virtual assets | Identify taxable vs. exempt activities

IFRS 15 / IAS 38 / IAS 2 | Recognition & measurement | Establish consistent financial reporting

Step | Transaction | IFRS Entry | VAT | CT

1 | EOR service delivered | Dr Crypto Asset 12,500 / Cr Revenue 12,500 | 5% on AED 12,500 | 9% CT on profit

2 | BTC value rises to AED 14,000 | Dr Crypto Asset 1,500 / Cr Other Income 1,500 | — | Taxable gain

3 | BTC sold for cash | Dr Bank 14,000 / Cr Crypto Asset 14,000 | — | —

1. Classify holdings correctly – IAS 2 vs. IAS 38.

2. Use fair value at transaction date for any crypto consideration.

3. Crypto payments don’t change VAT rules – still 5% on AED value.

4. Custodied crypto stays off-balance sheet.

5. Conversion gains are taxable income under UAE CT.

6. Maintain strong documentation – exchange rate source, time-stamp, wallet ID, transaction hash.

1. Can I issue a tax invoice in Bitcoin? No. VAT invoices must be in AED.

2. Do I pay VAT when exchanging Bitcoin for Dirhams? No. Exchange of virtual assets is VAT-exempt per VATP040.

3. What if I’m a Free Zone company? You can still qualify for 0% CT if you meet QFZP conditions.

4. Do I need a VARA licence if I just accept crypto payments? No. Only for those conducting crypto activities.

5. How should I value crypto received? Use a reputable exchange rate at the time of transaction.

6. Can I revalue crypto daily? You may, but IFRS requires revaluation at reporting dates unless you’re a broker-trader.

At Fastlane Tax & Accounting Consultancy, we help businesses across UAE — from VARA-licensed exchanges to regular companies accepting crypto — stay compliant with:

- IFRS-aligned accounting for digital assets (IAS 38 / IAS 2).

- VAT compliance under FTA VATP040.

- Corporate Tax optimisation and record-keeping for crypto income.

- Process design for audit-ready crypto invoicing and revaluation tracking.

Whether you’re an exchange, Web3 startup, or simply accepting crypto payments, Fastlane ensures your books, taxes, and compliance are 100% FTA-aligned — with zero penalty risk.