Corporate Tax Exemptions for Natural Resource Businesses

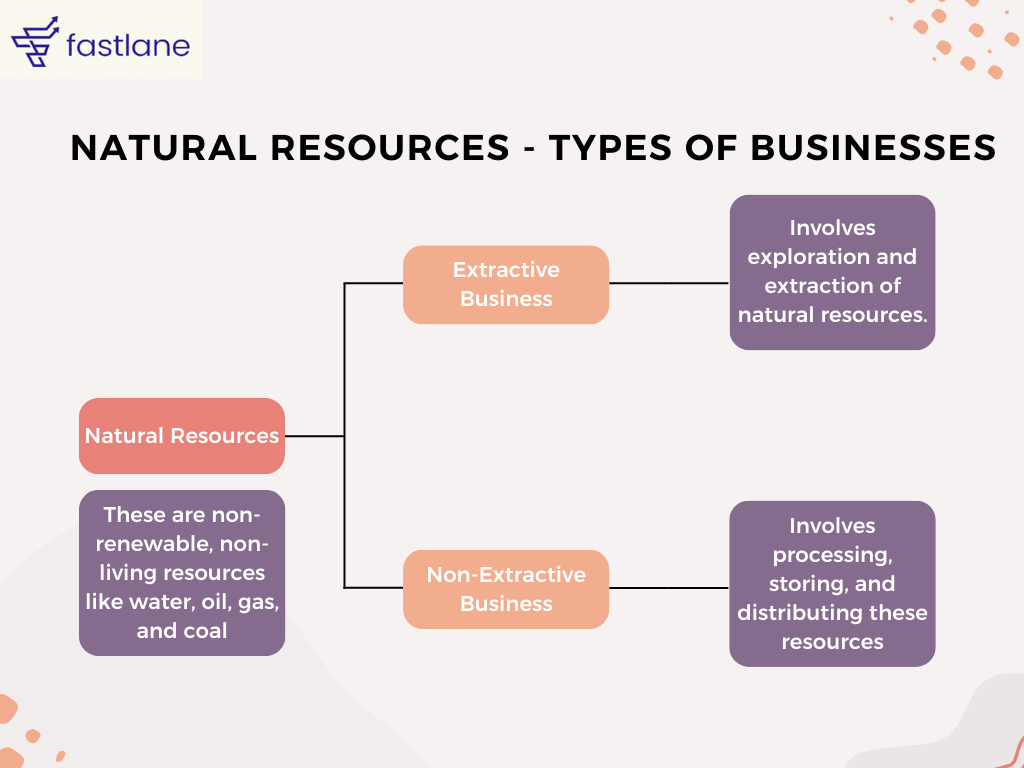

Natural resources in the UAE include non-renewable resources like water, oil, gas, coal, and minerals.

Extractive Businesses focus on exploring and extracting these resources, while Non-Extractive Businesses handle their processing, storing, and distribution.

Corporate Tax exemptions are available for these businesses if specific conditions are met.

What are Natural Resources?

Natural resources include water, oil, gas, coal, and naturally formed minerals.

These are non-renewable, non-living resources that can be extracted from the UAE’s land, territorial sea, and airspace.

Natural Resources do not include renewable resources such as solar energy, wind, animals, and plant materials.

What is an Extractive Business?

An Extractive Business involves exploring, extracting, removing, or otherwise producing and exploiting natural resources in the UAE.

Commonly referred to as the exploration and production sector, It includes upstream activities such as oil and gas extraction, mining, dredging, and quarrying.

What is a Non-Extractive Natural Resource Business?

Defined in the Corporate Tax Law as activities related to separating, treating, refining, processing, storing, transporting, marketing, or distributing the natural resources of the UAE.

Includes midstream and downstream activities in the oil and gas sector.

Taxation of Extractive Business and Non-Extractive Natural Resource Business

The Corporate Tax LAW, UAE exempts persons engaged in Extractive or Non-Extractive Natural Resource Businesses from Corporate Tax, recognizing the sovereignty of the Emirates over their natural resources.

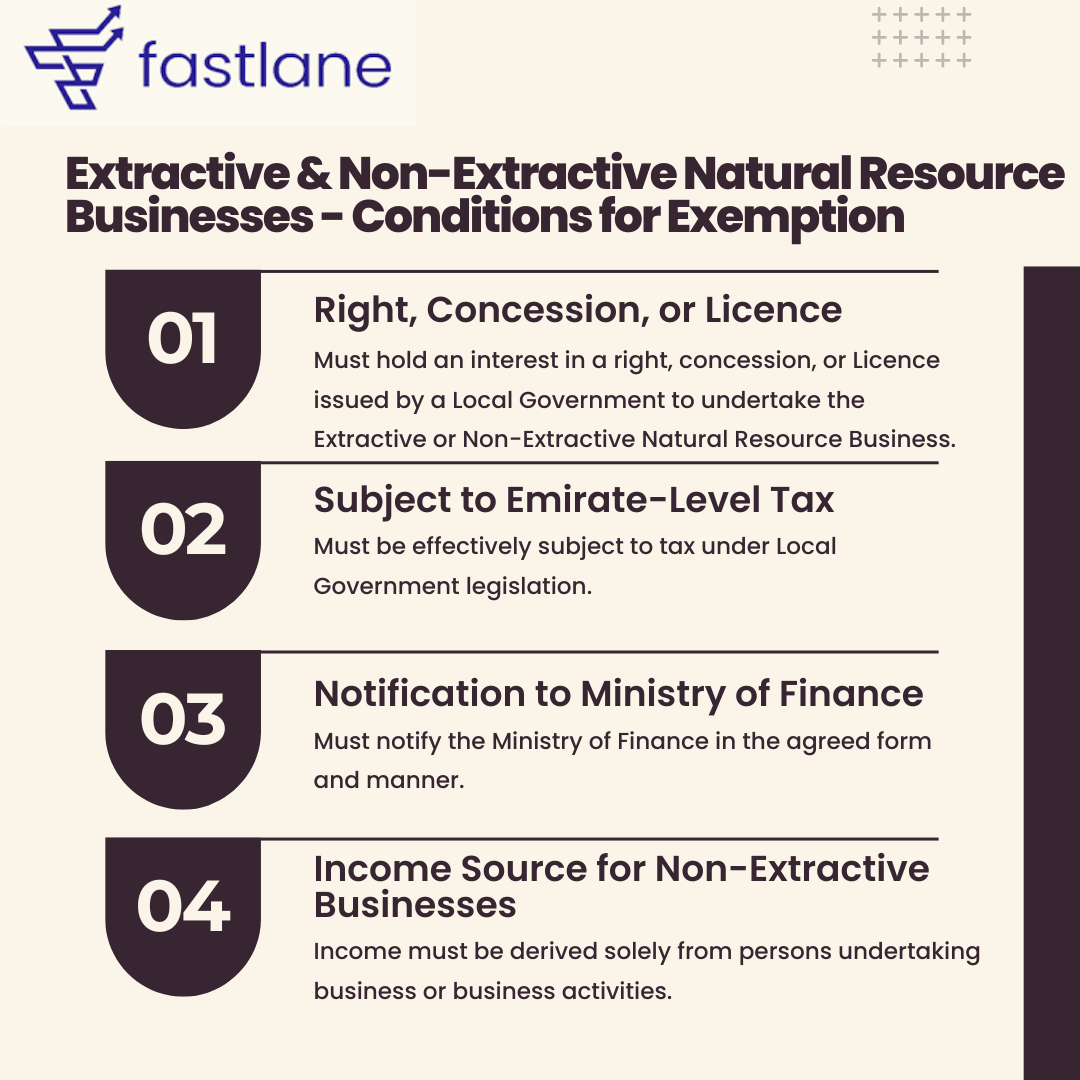

However, to qualify for this exemption, businesses must meet specific criteria outlined in the law. Primary Conditions:

Right, Concession, or License: The person must directly or indirectly hold an interest in a right, concession, or Licence issued by a Local Government to undertake the Extractive or Non-Extractive Natural Resource Business.

Subject to Emirate-Level Tax: The person must be effectively subject to tax under the applicable legislation of the Local Government.

Notification to Ministry of Finance: The person must notify the Ministry of Finance in the agreed form and manner with the Local Government.

Income Source for Non-Extractive Businesses: For Non-Extractive Natural Resource Businesses, income must be derived solely from persons undertaking business or business activity.

What is a right, concession, or License for a Natural Resource Businesses?

To qualify forCorporate Tax exemption, a person must directly or indirectly hold an interest in a right, concession, or License issued by a Local Government for Extractive or Non-Extractive Natural Resource Business.

This involves obtaining the relevant rights through procedures that vary between Emirates, often involving assignment, participation, or sub-participation agreements.

Practical Example

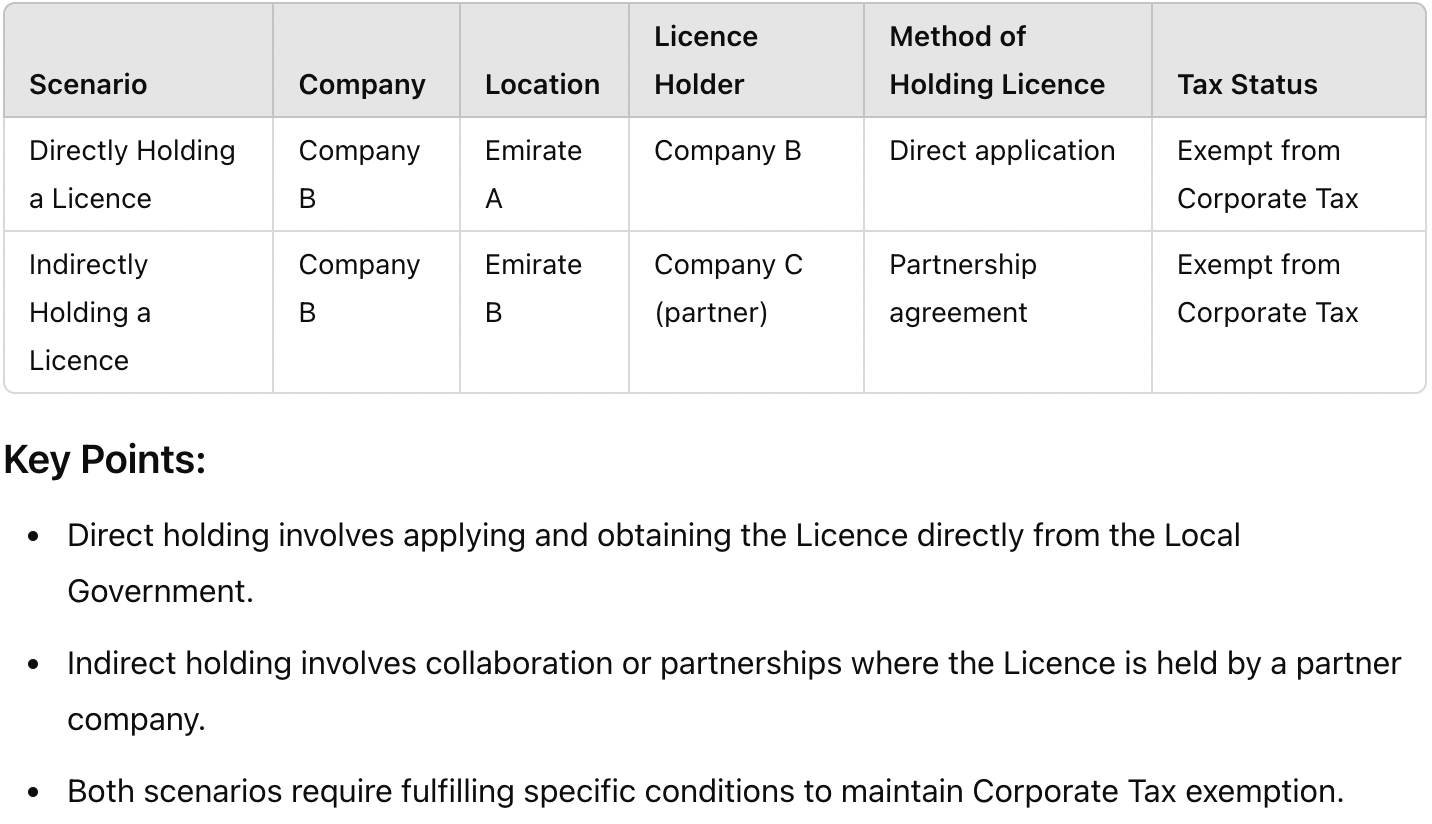

Scenario 1: Directly Holding a License

Company: Company B

Business: Mining of precious minerals

Location: RAK

Process:

Company B applies for a mining License from the Local Government of RAK.

After due process, Company B is granted the License.

Company B fulfills all conditions for the Corporate Tax exemption.

Outcome: Company B directly holds the License and is exempt from Corporate Tax for its operations in RAK.

Scenario 2: Indirectly Holding a License

- Company: Company B

- Business: Mining of precious minerals

- Location: Ajman

- Partner: Company C (holds a valid mining Licence in Ajman)

Process:

- Company B collaborates with Company C through a partnership agreement.

- Company B provides investment and technical expertise.

- Company C contributes its mining License and local knowledge.

- Company B gains a share of profits and is subject to Emirate B’s tax legislation.

Outcome: Company B indirectly benefits from Company C’s License and qualifies for Corporate Tax exemption in Ajman.

Subject to Emirate-level taxation to qualify for Corporate Tax exemption

To qualify for Corporate Tax exemption, a business must be effectively subject to tax under the legislation of the relevant Emirate.

This means the business is taxed by the Local Government, which could include income tax, royalties, or other fiscal measures.

Example

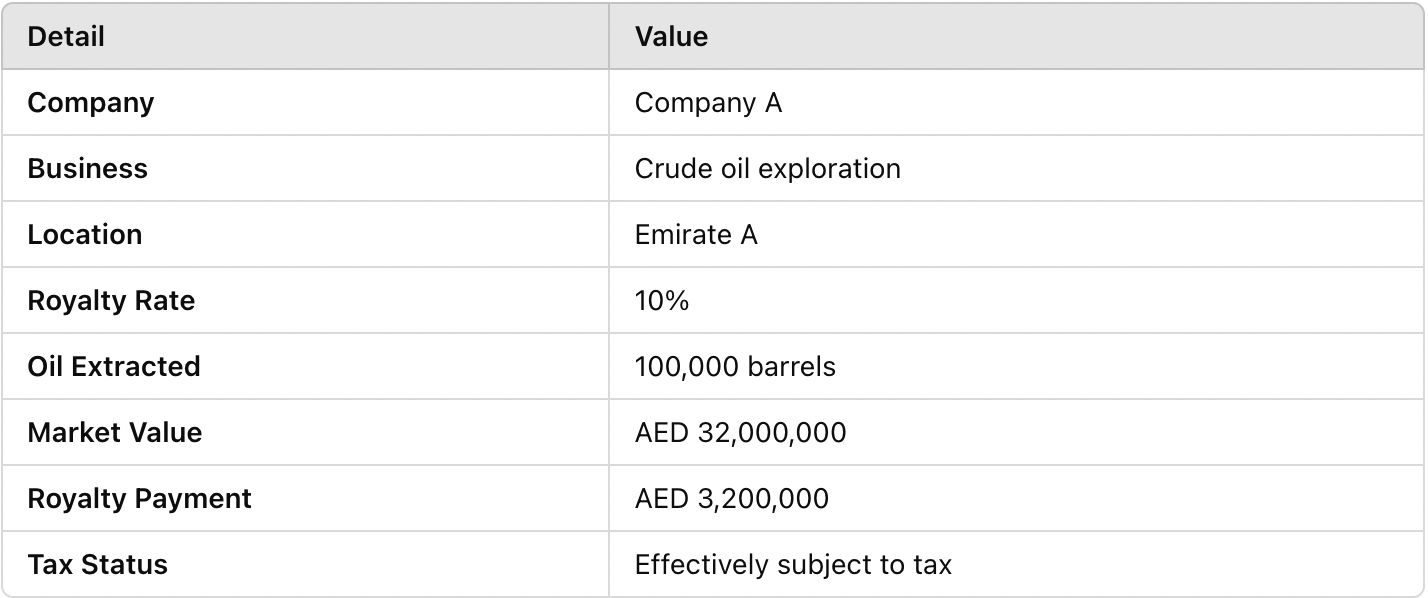

Scenario: Subject to Emirate-Level Taxation

Company: Company A

Business: Crude oil exploration

Location: Abu Dhabi

Agreement: Exploration and exploitation rights granted by Local Government

Taxation: Company A must pay a royalty for each barrel of oil extracted.

Royalty rate: 10% of the Market Value of the oil extracted.

Calculation:

- Period: 1 January to 31 December 2024

- Oil Extracted: 100,000 barrels

- Market Value: AED 32,000,000

- Royalty Payment: AED 3,200,000

Outcome:

Company A is considered effectively subject to tax at the Emirate level, meeting the requirement for Corporate Tax exemption.

Non-Extractive Natural Resource Businesses to derive Income solely from Persons undertaking Business or Business Activity for Corporate Tax exemption?

For Non-Extractive Natural Resource Businesses to qualify for Corporate Tax exemption, they must derive income solely from transactions with other businesses or business activities.

Engaging in transactions with end customers or consumers disqualifies them from the exemption.

Key Takeaways

1. Definition of Natural Resources: These are non-renewable, non-living resources like water, oil, gas, and coal that can be extracted from the UAE.

2. Types of Businesses:

- Extractive Business: Involves exploration and extraction of natural resources.

- Non-Extractive Business: Involves processing, storing, and distributing these resources.

3. Tax Exemption Conditions: Businesses must hold a right, concession, or Licence, be subject to Emirate-level tax, notify the Ministry of Finance, and derive income solely from business activities.

1. Ensuring Corporate Tax Compliance: - Help ensure your business is effectively subject to tax under the applicable legislation of the relevant Emirate.

2. Ministry of Finance Notifications: - Assist with the preparation and submission of notifications to the Ministry of Finance in the required form and manner. - Ensure that your business meets all the notification requirements to maintain tax exemption status.

3. Ongoing Compliance and Advisory:

- Provide regular updates and advisory on changes in the Corporate Tax Law and how they impact your business.

Created with

Login or sign up to start learningLogin to start learning