Corporate Tax Exemptions on Qualifying Investment Fund

What are Investment funds and Investment managers?

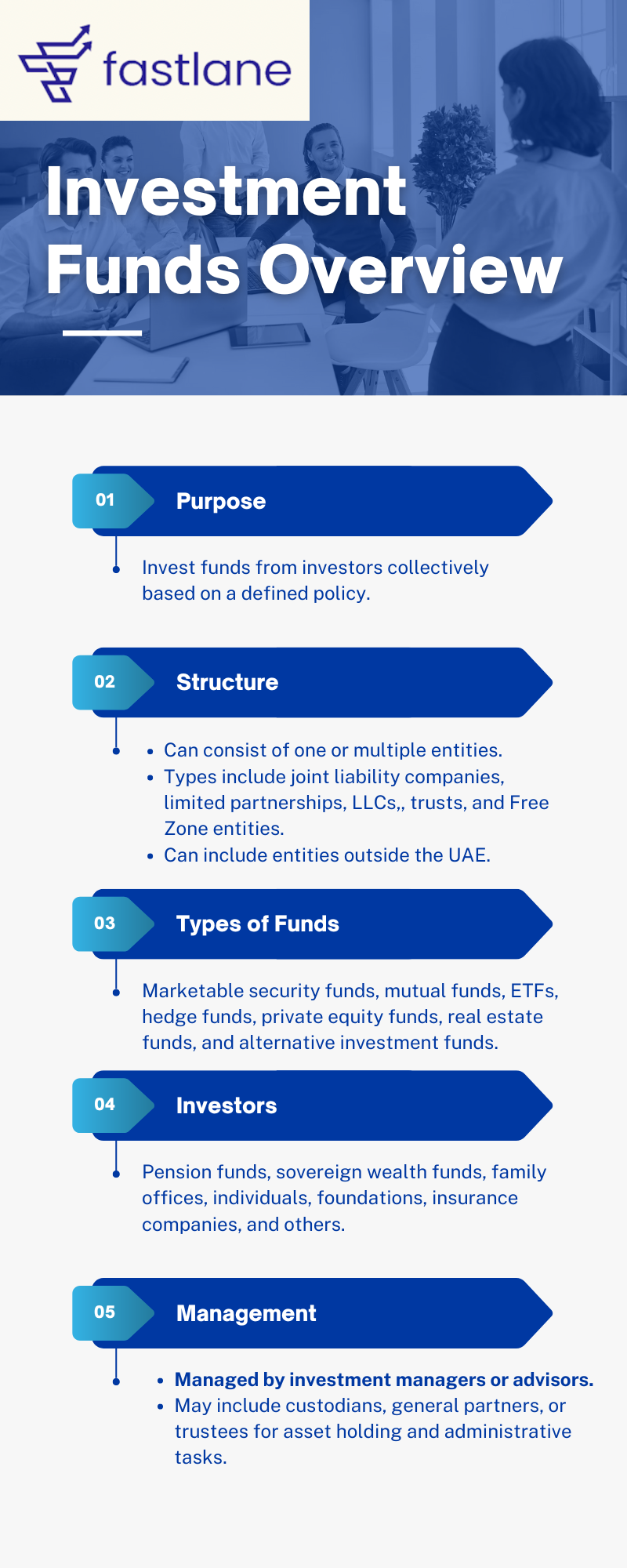

Investment funds pool funds from investors to invest collectively based on a defined investment policy, allowing investors to share in the profits. These funds can include various entities and operate in different forms, such as companies or partnerships, and may be based in the UAE or abroad. Common types of investment funds include mutual funds, hedge funds, and real estate funds.

Key Points 1. Structure and Types: Investment funds can be joint liability companies, limited partnerships, LLCs, public/private joint stock companies, or trusts. Common fund types: marketable security funds, mutual funds, ETFs, money-market funds, hedge funds, private equity funds, real estate funds, and alternative investment funds.

2. Investors and Capital: Investors, including pension funds, sovereign wealth funds, family offices, and individuals, provide capital for returns. The fund uses this capital for investments and business activities to generate profits.

3. Management: Funds may appoint Investment managers to make decisions per a pre-agreed policy. Managers or advisors might subcontract tasks to sub-advisors. Custodians or trustees may hold assets or perform administrative tasks.

4. Income and Fees: Investment managers earn through management fees, performance fees, or co-investments.

Fees are based on capital committed, invested, or assets managed, and can include a share of excess returns.

What is a Qualifying Investment Fund?

A Qualifying Investment Fund (QIF) in the UAE can apply for exemption from Corporate Tax if it meets specific conditions set out by the Corporate Tax Law.

Exempt from Corporate Tax: A QIF does not pay Corporate Tax once it qualifies and is approved for exemption.

Restrictions on Group Relief and Restructuring: The QIF cannot benefit from Qualifying Group Relief, Business Restructuring Relief, or the provisions for the transfer of Tax Losses.

Separate from Tax Group: The QIF cannot form part of a Tax Group.

Record-Keeping and Annual Declaration: The QIF must maintain records for at least 7 years and file an annual declaration to confirm it continues to meet exemption conditions.

Conditions for being a Qualifying Investment Fund

An investment fund can apply to the Federal Tax Authority (FTA) to be exempt from Corporate Tax as a Qualifying Investment Fund, provided it meets the conditions prescribed in Article 10(1) of the Corporate Tax Law and Cabinet Decision No. 81 of 2023.

Article 10(1) of the Corporate Tax Law Conditions:

- Regulatory Oversight Condition: The investment fund or its manager must be subject to the regulatory oversight of a competent authority in the UAE or a recognized foreign authority.

- Fund Ownership Condition: Interests in the investment fund must be traded on a Recognised Stock Exchange or be widely marketed and available to investors.

- Main Purpose Condition: The main or principal purpose of the investment fund should not be to avoid Corporate Tax.

Additional Conditions from Cabinet Decision No. 81 of 2023:

- Investment Business Condition: The main business activities must be investment business activities, with any other activities being ancillary or incidental.

- Diversity of Ownership Condition: - A single investor and its related parties should not own more than 30% of the fund if it has less than ten investors.

- They should not own more than 50% if the fund has ten or more investors.

- Investment Manager Condition: The fund must be managed or advised by an investment manager with at least three investment professionals.

- Independence Condition: Investors must not have control over the day-to-day management of the fund.

Conditions for Real Estate Investment Trusts (REITs)

The following additional conditions apply specifically to REITs, in addition to the conditions under Article 10(1) of the Corporate Tax Law:

- REIT Minimum Real Estate Asset Value Condition: The value of real estate assets (excluding land) under the management or ownership of the REIT must exceed AED 100 million.

- REIT Ownership Condition: - At least 20% of the REIT's share capital should be floated on a Recognised Stock Exchange, or

- It should be wholly owned by two or more institutional investors, with at least two of them not being related parties.

- REIT Real Estate Percentage Condition: The REIT must have an average real estate asset percentage of at least 70% during the relevant calendar year or the relevant 12-month period for which the financial statements are prepared.

Continuity of Conditions

If the conditions are not met continuously during the relevant tax period, the Qualifying Investment Fund or REIT might lose its status as an Exempt Person.

There are specific conditions under Article 4(6) of the Corporate Tax Law and Ministerial Decision No. 105 of 2023 that might prevent the immediate loss of status.

Impact of Not Meeting the Conditions in Later Tax Periods

If a Qualifying Investment Fund fails to meet any of the prescribed conditions during a Tax Period, it will cease to be considered an Exempt Person from the start of that Tax Period. This status change has several implications and specific exceptions:

Immediate Loss of Exempt Status:

General Rule: Once the conditions are not met, the fund will no longer be exempt from the start of the Tax Period in which the conditions were violated.

Exceptions to Immediate Loss of Status:

A Qualifying Investment Fund would not lose its exempt status from the start of the Tax Period if:

Liquidation or Termination:

The failure to meet the conditions results from the liquidation or termination of the fund.

The fund must notify the FTA within 20 business days from the start of liquidation or termination procedures.

The fund ceases to be an Exempt Person on the day after the completion of these procedures.

Temporary Non-Compliance:

The failure to meet the conditions is temporary and will be promptly rectified.

The fund must have procedures in place to monitor compliance.

Continuation as an Exempt Person:

To continue as an Exempt Person despite temporary non-compliance, the following conditions must be met:

Unpredictable or Unpreventable Situation: The failure must be due to an event beyond the fund's control, which it could not have reasonably predicted or prevented.

Application to the FTA:

The fund must apply to the FTA within 20 business days of failing to meet the conditions.

The FTA reviews and notifies its decision within 20 business days or another specified period.

Rectification Expectation:

The fund is expected to rectify the failure within 20 business days from the application.

This period can be extended by another 20 business days upon request and approval by the FTA.

Monitoring Compliance:

Upon FTA's request, the fund must provide evidence of procedures to monitor compliance within 20 business days or another specified period.

Consequences of Not Rectifying Conditions:

If the failure to meet the conditions is not temporary, the investment fund will:

Lose Exempt Status: Become a Taxable Person from the start of the Tax Period in which the conditions were not met.

Penalties for Non-Compliance: If the fund does not realize the conditions were not met and fails to file Tax Returns, it will be liable for penalties.

Impact on Wholly Owned Entities:

Entities wholly owned and controlled by the fund will also lose their Exempt Person status.

These entities will be subject to Corporate Tax if they are no longer continuously wholly owned and controlled by a Qualifying Investment Fund.

Investor Implications:

Investors in the fund who are Taxable Persons should exclude the relevant net income from their income as of the date of non-compliance.

Feeder funds and second investment funds must adjust their calculations for the Investment Business condition and diversity of ownership condition, respectively.

These measures ensure that investment funds maintain compliance to retain their exempt status, with structured protocols for addressing temporary lapses and significant penalties for prolonged non-compliance.

Taxation of Investment managers' fees

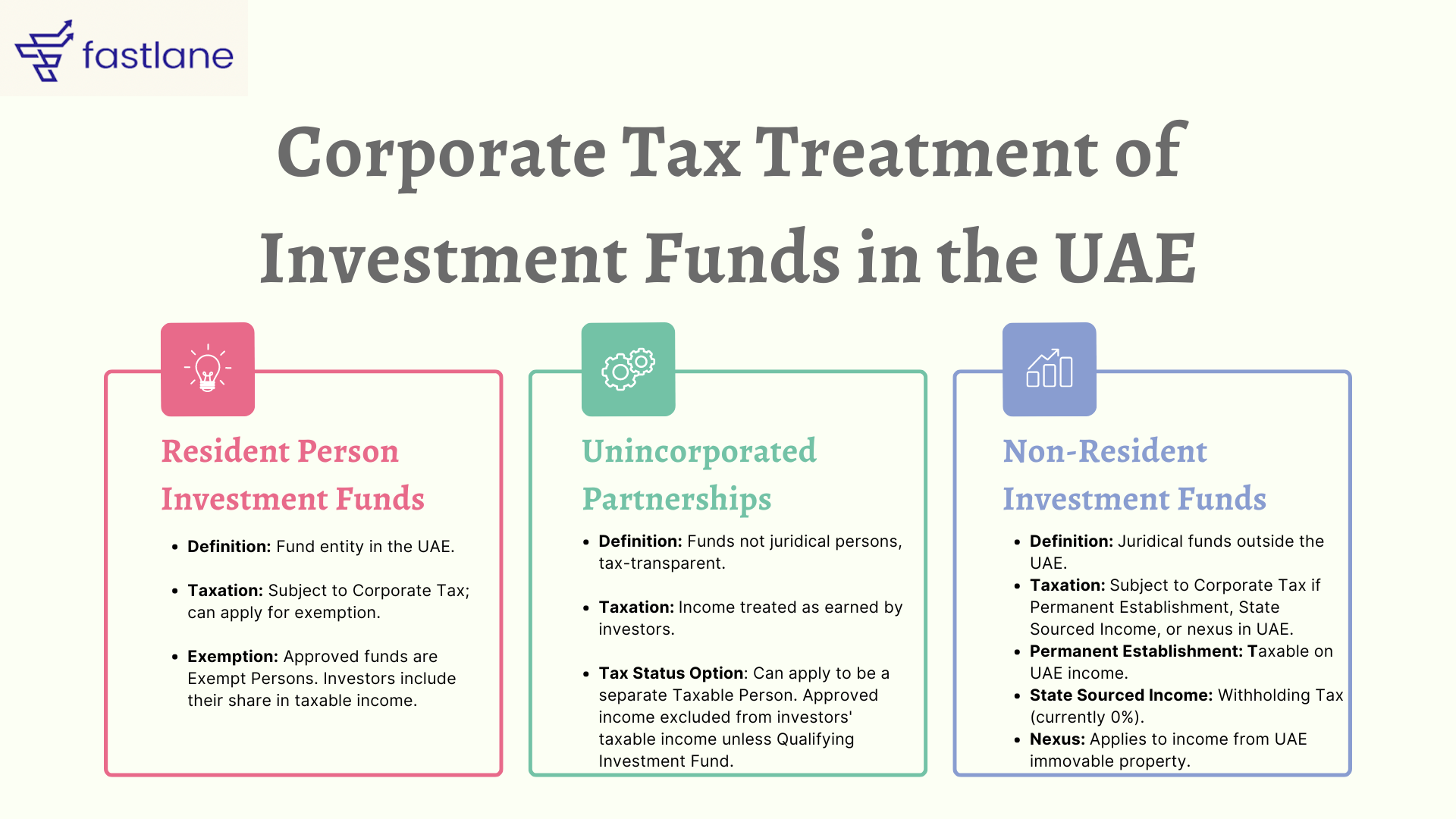

Investment managers' fees for brokerage or investment services are subject to UAE Corporate Tax if they are Resident Persons.

Non-Resident investment managers may also be taxed if they have a Permanent Establishment in the UAE or earn State Sourced Income, though the current Withholding Tax rate is 0%.

Key Takeaways

1. Diverse Structures and Types: Investment funds can take various forms, including companies, partnerships, and trusts. They can be based in the UAE or abroad, with common types such as mutual funds, hedge funds, and real estate funds.

2. Investor Roles and Capital: Investors, including pension funds and individuals, provide capital to investment funds, which use this capital to generate returns through various business activities.

3. Taxation of Funds and Managers:

- Resident Investment Funds: Subject to Corporate Tax but may be exempt if they qualify as a Qualifying Investment Fund.

- Unincorporated Partnerships: Income is taxed at the investor level.

- Non-Resident Funds: Taxed if they have a Permanent Establishment, State Sourced Income, or nexus in the UAE.

- Investment Managers: Fees earned are subject to Corporate Tax if they are Resident Persons or have a Permanent Establishment in the UAE.

1. Comprehensive Corporate Tax Guidance: - Fastlane provides tailored tax advice to ensure your investment fund benefits from available exemptions and favorable tax treatments

2. Ministry of Finance Notifications: - Assist with the preparation and submission of notifications to the Ministry of Finance in the required form and manner. - Ensure that your business meets all the notification requirements to maintain tax exemption status.

3. Ongoing Compliance and Advisory:

- Provide regular updates and advisory on changes in the Corporate Tax Law and how they impact your business.

Created with

Login or sign up to start learningLogin to start learning