How does Small Business Relief work for Corporate Tax, UAE

What is Small Business Relief?

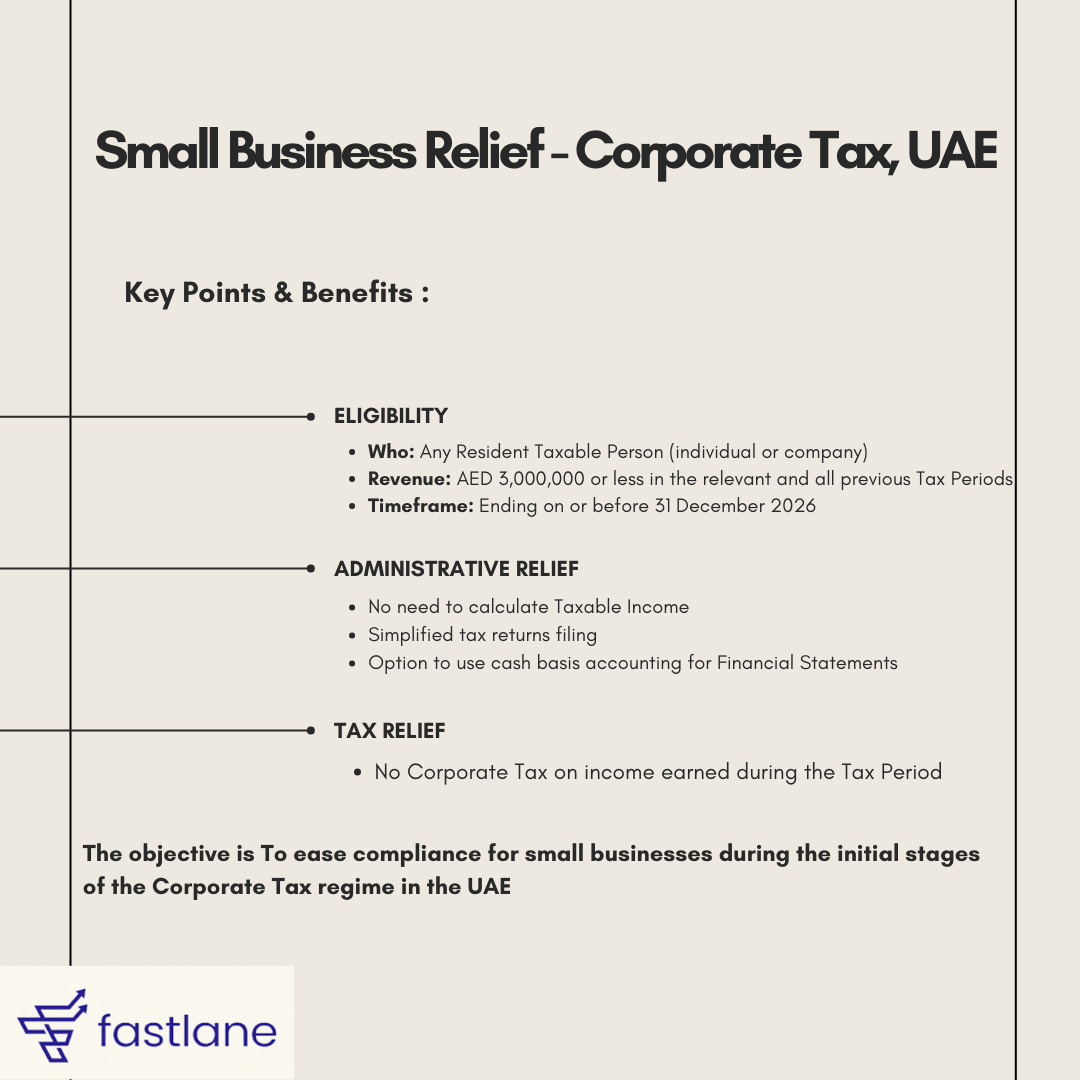

Small Business Relief is a measure to help small businesses in the UAE manage the Corporate Tax system more easily. It reduces the compliance burden by simplifying tax obligations for eligible businesses.

Key Points: - Eligibility : Any Resident Taxable Person (individual or company) with revenue of AED 3,000,000 or less in the relevant and all previous Tax Periods ending on or before 31 December 2026. Benefits:

Administrative Relief: Eligible businesses don’t need to calculate their Taxable Income and can file simplified tax returns. They can also use cash basis accounting for their Financial Statements.

Tax Relief: No Corporate Tax is required to be paid on income earned during the Tax Period.

This relief aims to make it easier for small businesses to comply with tax regulations during the early stages of the Corporate Tax regime.

How is Corporate Tax Calculated Under Small Business Relief ?

Small Business Relief allows eligible Resident Persons to elect to be treated as having no taxable income in a tax period where their revenue is less than or equal to AED 3,000,000.

As a result, they will pay no corporate tax for that period.

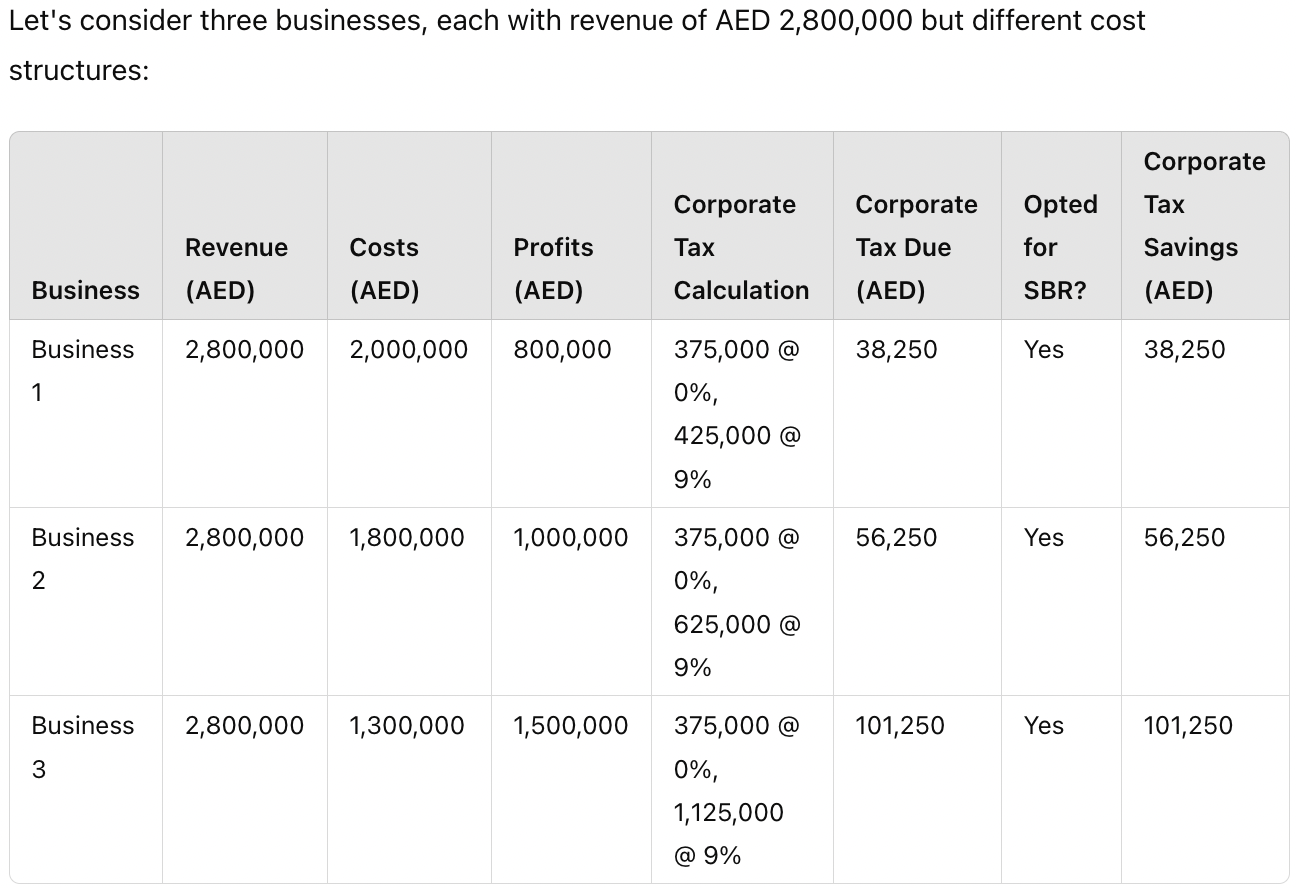

The amount of Corporate Tax liability that is not payable based on the relief will depend on the profitability of the business.

This is because Corporate Tax would be paid at the rate of 0% on taxable income up to AED 375,000 and 9% on taxable income above AED 375,000 had the Small Business Relief not been elected for.

This means that the amount of Corporate Tax relief enjoyed by businesses that are able to elect for Small Business Relief is relative to their profitability.

Example of Corporate Tax Calculation for entities opted for Small Business Relief

Eligibility Conditions for Small Business Relief in the UAE

Small Business Relief (SBR) in the UAE provides a valuable opportunity for eligible Resident Persons to minimize their corporate tax liabilities.

Eligibility Criteria

To qualify for Small Business Relief:

A person must be a Resident Person for Corporate Tax purposes.

The person must have Revenue of less than or equal to AED 3,000,000 in the relevant tax period and any previous tax periods.

Members of Multinational Enterprises (MNEs) and Qualifying Free Zone Persons are not eligible for SBR.

Restriction to Tax Periods: Small Business Relief is available for tax periods that begin on or after 1 June 2023 and end before or on 31 December 2026, provided the revenue criteria are met.

Example - Small Business Relief Eligibility

Example 1: Electing for Small Business Relief

Mr. X operates a business in Abu Dhabi and is a Resident Person for Corporate Tax purposes. He started trading on 1 January 2025, with his tax period ending on 31 December. In the tax period ending 31 December 2025, Mr. X's revenue was AED 2,000,000.

Outcome: Mr. X is eligible for Small Business Relief as his revenue is less than AED 3,000,000. He must elect for this relief in his tax return to benefit.

Example 2: Non-Resident Persons

ABC Ltd, a USA-incorporated company, has an office in Dubai to assist its UAE-based clients. It is a Non-Resident Person for Corporate Tax purposes. For the tax period ending 31 December 2024, ABC Ltd's revenue was AED 2,500,000, with AED 1,000,000 attributable to its Dubai office.

Outcome: ABC Ltd is not eligible for Small Business Relief as it is a Non-Resident Person, regardless of its revenue or having an office in Dubai.

How Can You Elect for Small Business Relief in the UAE?

Small Business Relief is an optional relief that must be elected within your tax return.

Once the tax return is submitted without electing for this relief, you cannot claim it later, so ensure you register with the FTA and obtain a TRN to make the election.

Key takeaways:

- Eligibility Criteria : Small Business Relief is available to Resident Taxable Persons (individuals or companies) with revenue of AED 3,000,000 or less in the relevant and all previous tax periods ending on or before 31 December 2026.

- Administrative and Tax Relief : Eligible businesses are exempt from calculating taxable income and can file simplified tax returns, alleviating compliance burdens.

- Tax Relief: No corporate tax is required to be paid on income earned during the tax period if the revenue criteria are met.

- Election Process : To benefit from Small Business Relief, businesses must meet specific criteria, and members of MNEs or Qualifying Free Zone Persons are not eligible for this relief.

Fastlane: Your Corporate Tax Partner : Fastlane provides expert guidance to ensure your business meets the eligibility criteria for Small Business Relief, assists in streamlined tax filing, and offers comprehensive compliance support to help you navigate the Corporate Tax system in the UAE.

Created with

Login or sign up to start learningLogin to start learning