Transfer Pricing (TP) is a fundamental component of corporate tax compliance in the UAE.

It ensures that transactions between related parties are conducted as if they were between independent entities, reflecting the true market value. This principle helps prevent profit shifting and ensures fair taxation.

Why does Transfer Pricing or Corporate Tax focus on Related Parties?

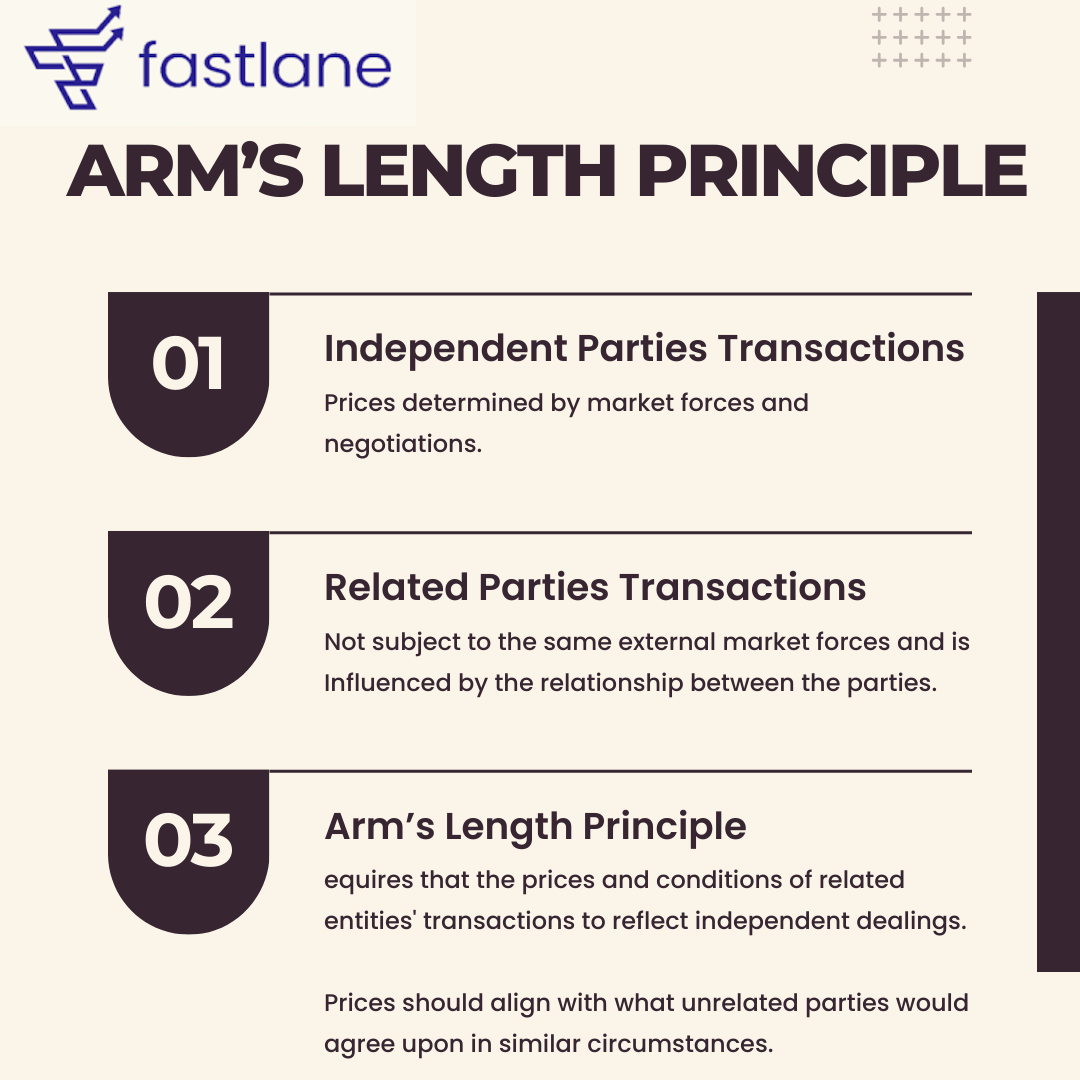

When independent parties transact with each other, the conditions of their commercial and financial relations (for example, the price of goods transferred, or services provided and the conditions of the transfer or provision) ordinarily are determined by market forces and negotiations.

On the other hand, Related Parties or Connected Persons may not be subject to the same external market forces in their dealings and may be influenced by the relationship between the parties involved.

Hence the Arm’s Length Principle of Transfer Pricing rules requires that the prices and conditions of transactions between related entities should reflect what would have been agreed upon if the entities were independent and dealing at arm's length. This means considering what price two unrelated parties would agree upon in similar circumstances.

What Are Related Parties?

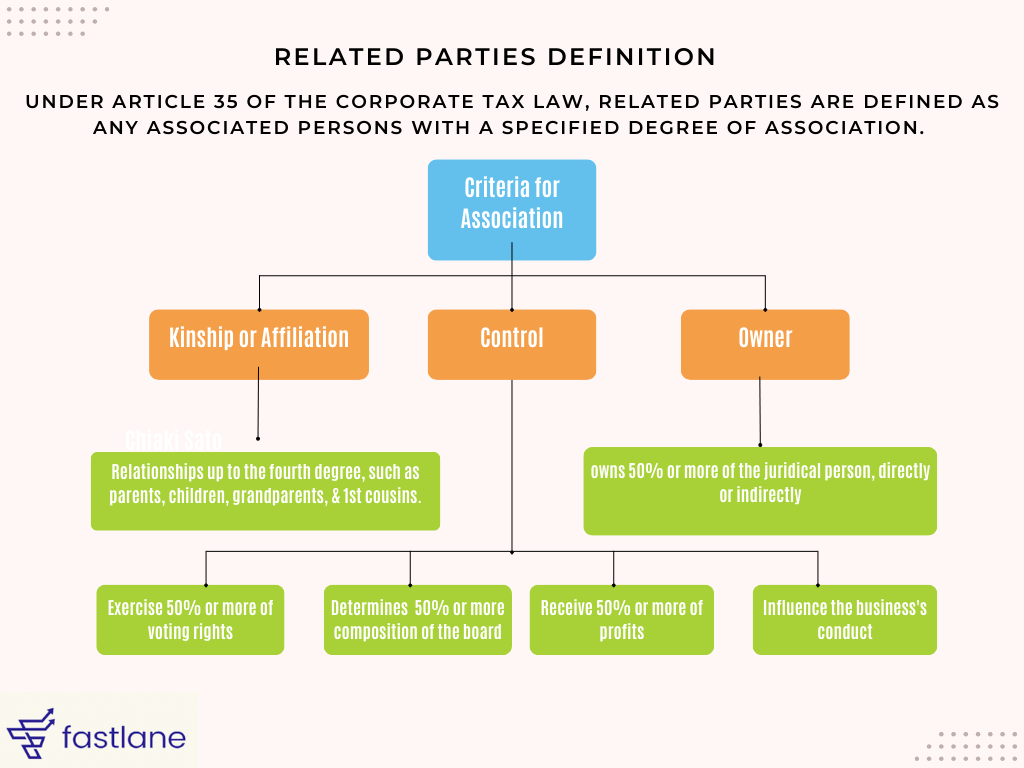

Under Article 35 of UAE Corporate Tax Law, A related party is someone or an entity that has a pre-existing relationship with another entity through ownership, control, or kinship.

Here's a quick rundown of what makes someone a related party:

Kinship or Affiliation

- Kinship: Two or more natural persons related up to the fourth degree. This includes parents, children, grandparents, grandchildren, siblings, uncles, aunts, nieces, nephews, and first cousins, among others.

- Ownership and Control: If a natural person or their related parties own 50% or more of another entity, or if they control the entity, they are considered related parties.

- Other Scenarios: Includes relationships like a person and their Permanent Establishment, partners in the same unincorporated partnership, and connections through trusts or foundations.

Control

Control means having the ability to influence another person or entity. This can be through:

- Voting Rights: Holding 50% or more of the voting rights.

- Board of Directors: Being able to determine 50% or more of the board's composition.

- Profit Sharing: Receiving 50% or more of the profits.

- Significant Influence: Exercising significant influence over the business and its affairs.

Connected Persons

Connected persons capture a broader group than related parties. This includes:

- Ownership Interest: A natural person who owns an interest in the taxable person.

- Directors and Officers: Individuals like managing directors.

- Relatives: Relatives of the above individuals.

Payments or benefits provided to connected persons are deductible only if they match the market value of the service or benefit and are incurred wholly and exclusively for business purposes.

Practical Example

Example 1: Family and Business Connections

Mr. B is a first cousin of Ms. C. Mr. B owns 75% of B LLC. Ms. C owns 20% of C LLC but has 60% of the voting rights due to preferential shares. They are also partners in an unincorporated partnership with D Ltd.

Mr. B and Ms. C: Related parties due to kinship.

Mr. B and B LLC: Related parties due to ownership.

Mr. B and C LLC: Connected persons because Ms. C controls C LLC.

Ms. C and C LLC: Related parties due to control.

Ms. C and D Ltd: Related parties as partners in the same partnership.

B LLC and D Ltd: Unrelated juridical persons.

Ms. C and B LLC: Connected persons through family relationship with Mr. B.

Transfer Pricing

Transfer pricing ensures transactions between related parties and connected persons are priced as if they were between independent parties. This prevents artificial profit shifting. Taxable persons must comply with transfer pricing disclosure requirements and maintain records to prove their transactions follow the arm's length principle.

How Fastlane Can Help

Navigating the complexities of related parties and transfer pricing can be challenging, but Fastlane is here to help. We offer 'Smart Compliance' solutions to manage your corporate tax obligations smoothly.

Our services include:

-

Transfer Pricing Study - Advising on related party transactions.

- Ensuring compliance with transfer pricing rules.

- Handling disclosure requirements and documentation.

With Fastlane, you can focus on growing your business while we take care of the intricate details of corporate tax compliance. Schedule a free consultation with us to see how we can help your business thrive in the UAE.