What Foreign Income is Exempt for Companies under UAE corporate tax law?

Introduction

If your UAE-based company owns stakes in foreign

businesses, you might be paying more tax than required—or

worse, missing out on valuable exemptions.

Under UAE Corporate Tax Law, businesses can benefit from

the Participation Exemption, which allows dividends and

capital gains from foreign subsidiaries to be tax-free—if certain

conditions are met.

But what are these conditions? And how can businesses ensure

maximum tax efficiency while staying compliant?

Let’s break it down.

Understanding Participation

Exemption on Foreign Income

Participation Exemption applies to foreign

dividends and capital gains, allowing UAE businesses to avoid

double taxation on profits earned outside the country. However, not

all foreign income qualifies.

Key Conditions to Qualify for the Participation

Exemption

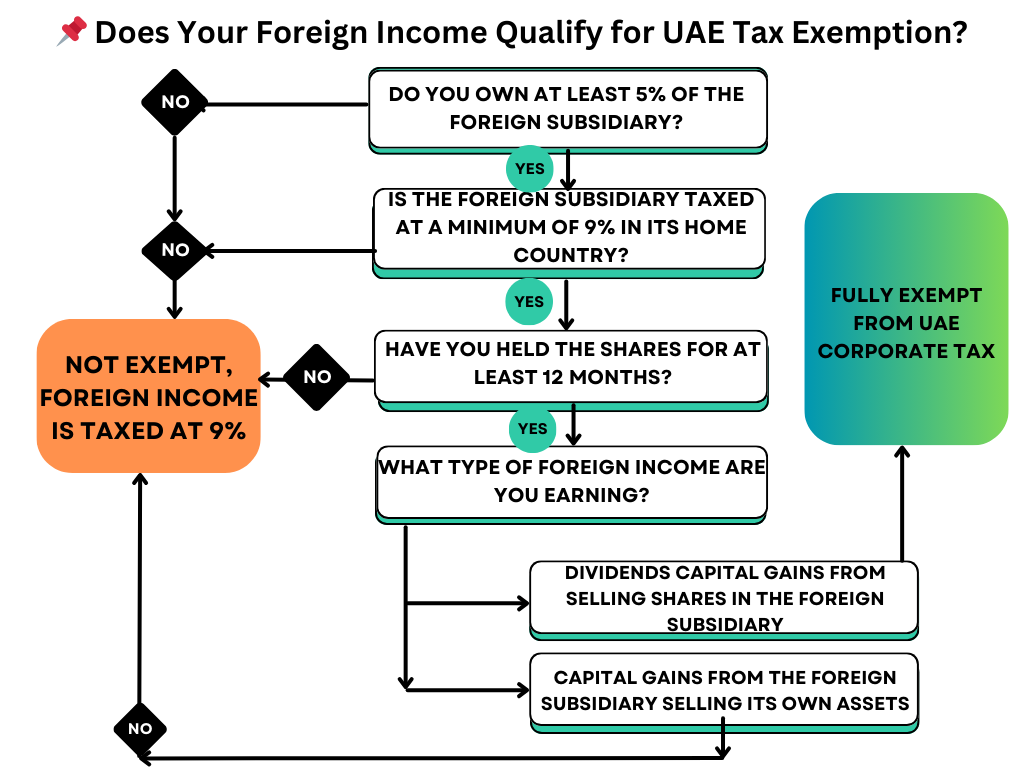

✅Minimum Ownership:

Your UAE company must own at least 5% of the foreign subsidiary

OR meet the minimum acquisition cost test. ✅Foreign Tax Rate:

The foreign subsidiary must be subject to at least 9% corporate tax

in its home country. ✅Holding Period:

No strict requirement exists, but a stable ownership structure

strengthens the exemption. ✅Free Zone Status:

The exemption applies to both mainland UAE and Free Zone entities.

✅ If you passed all 3 conditions (5% ownership, 9% foreign tax, 12-month holding), your dividends & capital gains (from selling shares) are tax-free. ❌ If you missed any condition, your foreign income is taxed at 9%.

Now, let’s explore real-world scenarios to

understand how this works.

Scenario 1: The Cost of a Low

Foreign Tax Rate

Company X (UAE) owns 12% of a foreign

subsidiary that is subject to a 15% corporate tax. The

subsidiary sells an asset, making AED

2 million in capital gains, and then

distributes AED 1 million in

dividends.

Tax Treatment in UAE:

✅Dividend is fully exempt

– because the foreign subsidiary meets the 9% tax threshold and ownership

is above 5%. ❌Capital gain is taxable

– because the Participation Exemption does not cover capital gains

unless the UAE company sells its shares in the subsidiary.

Lesson Learned:

Not all foreign income qualifies for tax exemption. Dividends are

exempt, but capital gains depend on how they are realized.

Scenario 2: Holding Period

Matters!

Company Y (UAE) owns 20% of a foreign

subsidiary for just 6 months. The subsidiary is

taxed at 12% and

pays AED 2 million in dividends.

Tax Treatment in UAE:

❌Dividend

is fully taxable – because the UAE company has not held the shares for at least 12 months.

Lesson Learned: Even if the foreign tax rate is above 9% and ownership is above 5%,

the holding period is

crucial. To benefit from the exemption, you must own the shares for

at least 12 months.

Scenario 3: When Capital

Gains Are Exempt

Company Z (UAE) sells its 7% stake in a foreign subsidiary after 3

years. The foreign subsidiary is taxed at 18%, and the UAE company makes AED 4 million in capital gains.

Tax Treatment in UAE:

✅Fully

exempt under Participation Exemption –

because:

·The ownership exceeds 5%.

·The foreign tax rate is above 9%.

·The shares were held for more than 12 months.

Lesson Learned: If you sell shares

in a qualifying foreign subsidiary, the capital gain is also exempt under the Participation Exemption.

Scenario 4: The Danger of

Low-Tax Jurisdictions

Company A (UAE) owns 60% of a foreign

subsidiary that pays only 5% corporate tax. The

subsidiary distributes AED 3 million in

dividends.

Tax Treatment in UAE:

❌Dividends

are fully taxable at 9% – because the foreign tax rate is below 9%.

Lesson Learned: Simply owning more

than 5% of a subsidiary does not guarantee exemption. The foreign

corporate tax rate must be 9% or higher.

Key Takeaways

✔️Foreign dividends can

be fully exempt, but only if the foreign subsidiary pays at least 9% corporate

tax. ✔️Capital gains are

exempt only when the UAE company sells its shares—not when the foreign

subsidiary sells its assets. ✔️Holding period of 12

months is critical to claim the exemption. ✔️Subsidiaries in low-tax

jurisdictions (less than 9%) do not qualify for exemption, and their dividends

are taxed at 9%.

-Losses from a

qualifying participation interest cannot be deducted under UAE Corporate Tax. ✔️If a subsidiary delays

dividends, the exemption is assessed at the time of distribution, based on

compliance with exemption conditions.

How Fastlane Can Help

Navigating UAE corporate tax laws and optimizing

foreign income taxation can be complex. Fastlane’s tax experts

can help you: ✅Structure foreign

investments for maximum tax efficiency. ✅Ensure compliance with

Participation Exemption rules. ✅Avoid unnecessary

taxation on foreign dividends and capital gains.

🔹Want to minimize

your corporate tax liability while staying 100% compliant? Get a free

consultation with our experts today! 🚀

Created with

Login or sign up to start learningLogin to start learning