Demiminis Requirement for Free Zone Persons in UAE:

Understanding the Criteria with a Case Study

Introduction

Free Zone Persons in the UAE benefit from a 0% corporate

tax rate on qualifying income, provided they meet the conditions outlined

in the UAE Corporate Tax Law. One critical requirement is the Demiminis Rule,

which determines whether a Free Zone Person qualifies for tax incentives.

In this blog, we’ll break down the step-by-step calculation

of the Demiminis Requirement, analyze a case study, and highlight

key takeaways. By the end, you’ll understand whether your Free Zone business

meets the qualification criteria and how Fastlane Consultancy can assist

in ensuring compliance.

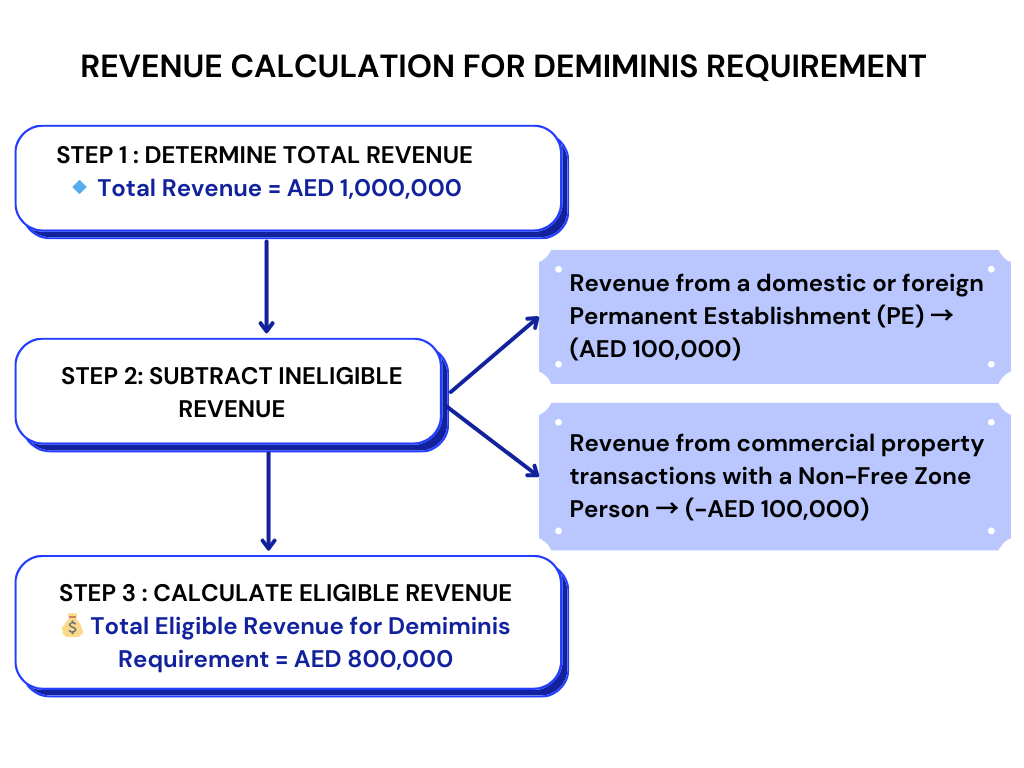

Step 1:

Calculate Revenue for the Demiminis Requirement

The first step is to determine the revenue that qualifies

for the Demiminis Requirement by excluding certain types of revenue.

Let's assume the total revenue for the period is AED

1,000,000.

Total Revenue for the Demiminis Requirement = AED 1,000,000 – (100,000 + 100,000) = AED 800,000

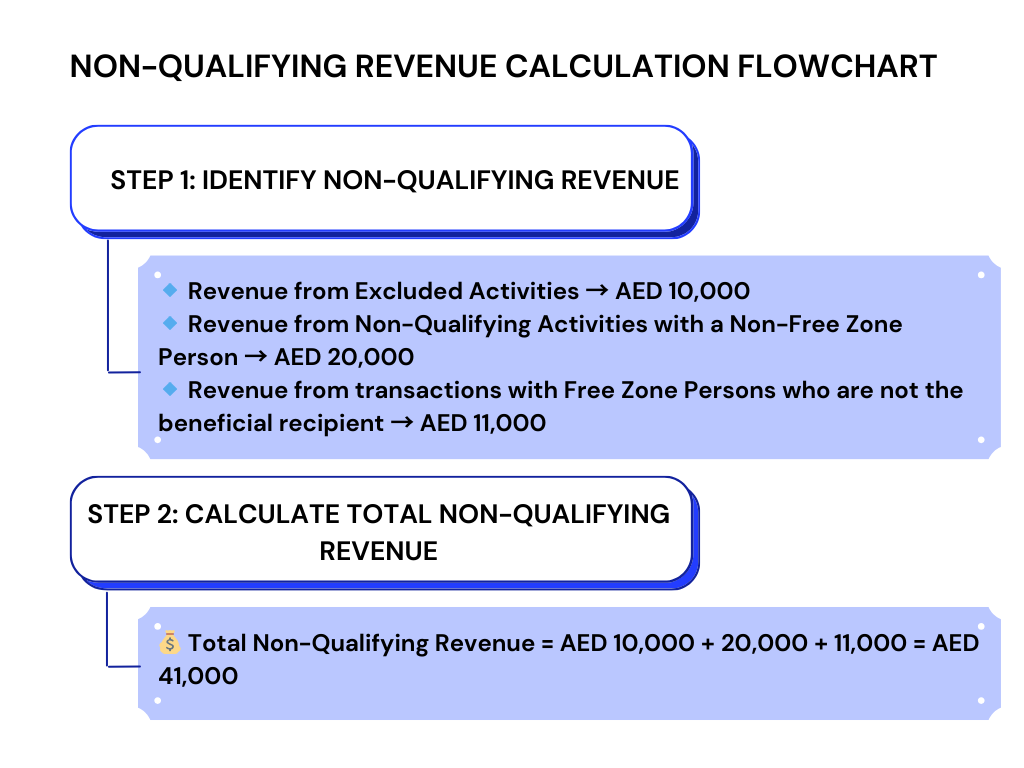

Step 2:

Calculate Non-Qualifying Revenue

Next, we identify revenue that does not qualify under the

Free Zone tax incentives:

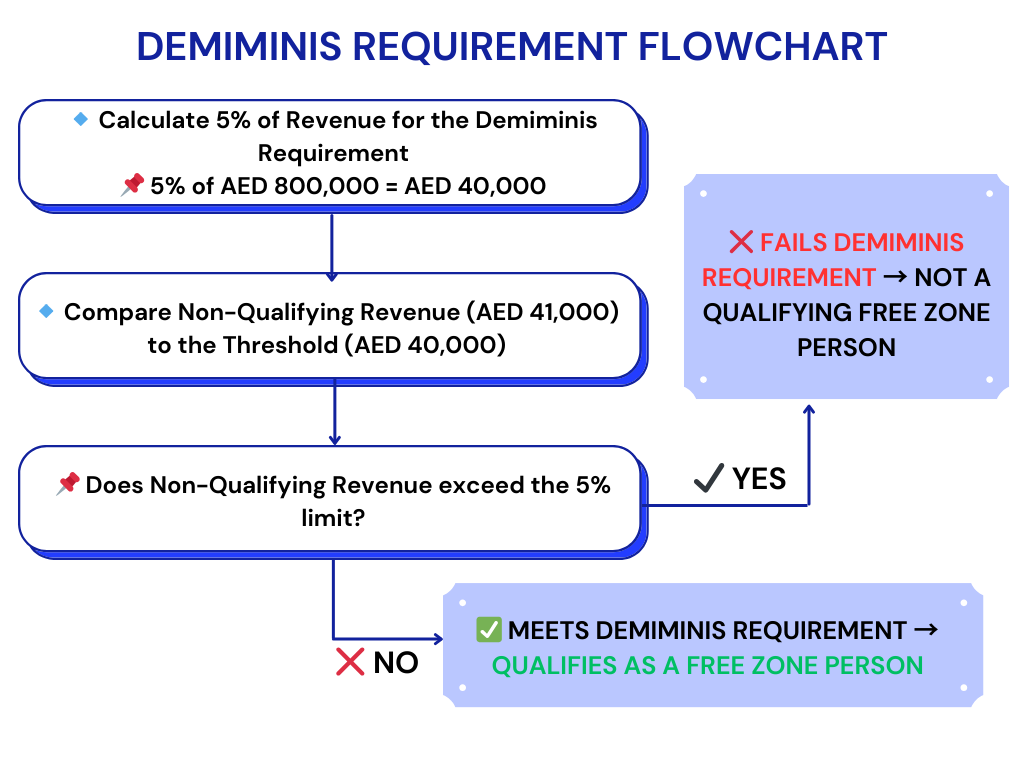

Step 3: Does

the Free Zone Person Meet the Demiminis Requirement?

The Demiminis threshold states that Non-Qualifying Revenue

must not exceed 5% of the revenue for the Demiminis Requirement or AED

50 million, whichever is lower.

5%

of AED 800,000 = AED 40,000

Total

Non-Qualifying Revenue = AED 41,000

Since Non-Qualifying Revenue (AED 41,000) exceeds the 5%

threshold (AED 40,000), the Free Zone Person does not meet the Demiminis

Requirement and will not be considered a Qualifying Free Zone Person.

What Happens

If the Requirement is Met?

Now, let’s consider a second scenario where Non-Qualifying

Revenue is AED 40,000 instead of AED 41,000.

5%

of AED 800,000 = AED 40,000

Total

Non-Qualifying Revenue = AED 40,000

Since the Non-Qualifying Revenue is within the allowable

limit, the Free Zone Person qualifies as a Qualifying Free Zone

Person.

Step 4:

Determine Qualifying Revenue for 0% Taxation

Once the Demiminis Requirement is met, the next step

is to assess the Qualifying Revenue that will be taxed at 0%.

Revenue

derived from Free Zone Persons (excluding income from Excluded Activities) = AED 600,000

Revenue

derived from Non-Free Zone Persons in respect of Qualifying Activities = AED 160,000

To validate this, we check whether:

Total Revenue for Demiminis Requirement = Total

Non-Qualifying Revenue + Total Qualifying Revenue

Revenue

from Non-Free Zone Persons (Qualifying Activities) = AED 160,000

Total

= AED 760,000

Since the values align, the Free Zone Person qualifies

for the 0% corporate tax rate on the AED 760,000 Qualifying Revenue.

Key

Takeaways

The

Demiminis Requirement ensures that only Free Zone entities with

minimal Non-Qualifying Revenue benefit from the 0% corporate tax rate.

Non-Qualifying

Revenue must not exceed 5% of the Demiminis Revenue or AED 50 million—whichever is lower.

If

the requirement is not met, the Free Zone Person loses the tax

benefits.

If

the requirement is met, only Qualifying Revenue will be subject to 0%

corporate tax, while other income will be taxed at the standard 9%

rate.

Accurate

revenue categorization is crucial to maintain Free Zone tax benefits.

How Fastlane

Consultancy Can Help

Navigating UAE corporate tax compliance can be

complex, especially with regulations like the Demiminis Requirement. Fastlane

Consultancy specializes in:

✔Assessing your Free Zone tax

status ✔Accurate revenue classification ✔Ensuring compliance with corporate tax laws ✔Filing tax returns and advisory services

Get in touch with us today

to ensure your Free Zone business remains compliant and maximizes its tax

benefits. 🚀

Created with

Login or sign up to start learningLogin to start learning